Where Does T-Mobile Fit in Goldman's Consumer Strategy?

Starling's Bounce Back Loan Fraud, LendUp/Kinly/Bancorp Update, Walmart Readies ONE, Citi Exits UK Retail Market

Hey all, Jason here.

I made it back safe and sound to the Netherlands last Sunday — just a day before a 7.6 magnitude earthquake rocked México. Oddly enough, it struck on the same day, September 19th, as prior quakes in 1985 and 2017. If you have friends or family in the region, I hope they’re all safe and recovering from the disaster.

My Money20/20 calendar is already beginning to fill up! If you’re interested in meeting up, drop me a line here. Also, don’t forget that I’ll be co-hosting a happy hour Tuesday evening with my friends at Performline — you can RSVP here.

Existing subscriber? Please consider supporting this newsletter by upgrading to a paid subscription. New here? Subscribe to get Fintech Business Weekly each Sunday:

SMB Lenders: Better Data Means Higher Approval & Repayment Rates

Sponsored content: Despite the advances fintech has brought to small business lending, too often data remains balkanized and processes remain manual — resulting in higher operating expenses and missed opportunities.

Uplinq’s global solution utilizes billions of alternative data sets and incorporates environmental, market & community data, as well as having direct integrations with core banking providers, credit bureaus, rating agencies, accounting systems and other permissioned and non-permissioned sources. The data sets have served as a foundational component for over $1.4 trillion in underwritten loans, while delivering the following outcomes:

Increased Loan Approval Rates

Mitigated Loan Risk

Improved Customer Relations

Increased Net Income

Uplinq’s technology has previously helped major FIs like Chase, Citibank and Itaú, as well numerous non-bank lenders turn around negative ROA portfolios while significantly transforming their small business loan portfolio.

Where Does T-Mobile Fit in Goldman’s Consumer Strategy?

Last week, Bloomberg reported that Goldman Sachs and T-Mobile have reached an agreement for the bank to power a T-Mobile credit card program. The mobile carrier would be Goldman’s third credit card partner, joining Apple and automaker GM.

T-Mobile, now the US’ second-largest mobile carrier after its merger with Sprint, may have been an attractive target because, unlike competitors Verizon and AT&T, T-Mobile doesn’t presently offer a cobranded credit card. Goldman didn’t need to win this business from a competitor, like with GM, which Goldman poached from Capital One.

T-Mobile boasts some 88 million subscribers that can be targeted with credit card offers, though the company has long catered to users with lower incomes or checkered credit histories. Based on recent filings, 38% of T-Mobile’s outstanding receivables are from customers rated subprime by the company’s scoring model.

Partnering with subprime-heavy T-Mobile may raise a few eyebrows, given recent analysis showing loss rates on Goldman’s existing credit card portfolio nearly hitting 3%, which one JPMorgan analyst described as “well above subprime.”

Recent filings show 28% of Goldman’s current credit card lending — mostly to Apple Card users — is to consumers with FICO scores of 660 or lower. That’s a significantly higher percentage than Goldman’s Marcus-branded installment loans, where less than 5% of outstanding balances are held by consumers with a sub-660 score.

So what, exactly, might Goldman’s strategy with its card cobrand partners be?

Card Issuers’ Cobrand & Private Label Strategies

Looking at major card issuers’ strategies historically, you can roughly break them into three groups.

First, there are major card issuers like Chase and American Express, which primarily issue their own-branded cards, but also parter with select, high-value consumer brands. For instance, Chase issues cobrand cards for United Airlines, Marriott Hotels, and Disney. Amex offers Delta and Hilton cobrands.

The second group focuses its business primarily on issuing cobranded cards, and may or may not issue cards under its own name. Barclays (in the US) and FNBO exemplify this approach. Barclays powers 20+ cobrand cards, including for companies as varied as Emirates, the AARP, Barnes & Noble, and Old Navy. FNBO claims to issue cards for over 250 partners, including Ford, MGM, and Verizon Business.

The last group focuses on issuing private label cards (“store cards”) as well as cobranded cards. Major players in this space include Synchrony, which issues private label cards for retailers like American Eagle, Chevron, and TJ Maxx, as well as cobrand cards for PayPal/Venmo and Verizon.

Bread Financial (formerly Comenity/Alliance Data) is also a big player, offering private label cards for Abercrombie & Fitch, Forever21, and GameStop, as well as cobrand cards for Victoria’s Secret and the NFL.

Citibank is somewhat unique in that it is a major issuer across all categories: its own-branded cards, cobranded (American Airlines, Costco, Macy’s), and private label (Home Depot, Wayfair, Best Buy).

What Path is Goldman On (And Why)?

Assuming news of the T-Mobile deal is accurate, how should we think about Goldman’s evolving credit card efforts?

It’s notable that the firm hasn’t introduced its own credit card under the Marcus brand. And, with reports that Goldman may push its already-delayed Marcus checking into 2023 to save on the expense of marketing it, a Marcus credit card seems extremely unlikely in the near future.

With little chance it will launch its own card, Goldman’s strategy looks more like Barclays or FNBO — leaning on brands aligned with a wide variety of consumer segments — than it does like Chase or Amex.

While the economics between issuer and cobrand partner vary with program design, one potential motivation for Goldman may be to outsource the marketing effort (and expense) to its partners, who then would likely be compensated per newly opened account and/or on a rev-share basis.

Such an approach makes all the more sense for brands that have large, engaged customer bases — more the case for Apple and perhaps T-Mobile than GM.

T-Mobile has easy access to market to its 88 million customers via email, text message, and direct mail — as well as being able to use its vast data to target customers across digital channels.

Further, T-Mobile has something even Apple didn’t when launching its card with Goldman — credit data of its existing customers. This can be used to more effectively target credit card offers to its customer base.

On top of data T-Mobile may have pulled from bureaus, it also has proprietary credit data — its users’ payment history with the carrier. This has the potential to serve as a supplementary data source to help underwrite customers who otherwise might not fit Goldman’s credit box.

T-Mobile also boasts something wireless competitors and Goldman’s other credit card cobrand partners lack: its own neobank. The carrier launched the product, powered by BM Technologies and Customers Bank, in 2019.

The existing T-Mobile MONEY user base could be an interesting segment to market to — though users of similar mass-market neobanks like Chime or Varo tend to skew lower income and lower credit score or thin/no file.

It’s unknown whether the reported T-Mobile/Goldman credit card offering would be integrated into the existing T-Mobile MONEY app, with users applying for cards and servicing their account through the app (akin to how Goldman works with Apple), or if applications and servicing would be handled via Marcus’ app and site, as is the case for GM cards.

No Guarantee of Success

T-Mobile’s large customer base doesn’t guarantee the successful launch of a cobrand card.

Uber, which boasts tens of millions of riders in the US, launched a cobrand card with Barclays in November, 2017. Despite tinkering with the rewards structure, the card was never able to achieve significant traction, and the program was canceled in June, 2021.

Rideshare competitor Lyft, which was working on a card offering with Synchrony, killed the project before it even launched.

Still, T-Mobile has proven itself to be a savvy dealmaker and marketer in the past.

Its “uncarrier” product and marketing strategy cleverly differentiated itself from legacy stalwarts AT&T and Verizon by focusing on notorious customer pain points: contracts, early termination fees, “hidden fees” (taxes and surcharges), and bad customer service. T-Mobile’s “uncarrier” philosophy is well-aligned with how Goldman has positioned Marcus, where it has emphasized “no-fee” offerings and good customer service.

However, unlike Goldman’s GM deal, the bank won’t inherit any existing cardholders. And a T-Mobile-branded credit card is unlikely to attract the kind of rabid fanboy excitement the Apple Card did.

The success of the partnership is likely to boil down to two interlinked factors: the efficacy of T-Mobile’s marketing efforts and Goldman Sachs’ credit risk management.

It’s unlikely Goldman will break out data on its card programs by partner, which will make it difficult if not impossible to assess the performance of specific cobrand deals.

Still, the metrics to keep an eye on, if and when the T-Mobile partnership goes live, include, of course, the number of customer accounts and outstanding balances, but also the share of Goldman’s portfolio that is sub-660 and any impact on delinquency and charge off rates.

Update: Bancorp’s Dubious Response to Kinly’s Issues

First, a quick recap.

When LendUp was facing existential regulatory threats to its payday lending business, it attempted a last-ditch pivot: starting a neobank called Ahead Money.

While the company was able to get the project live, it’s unclear how many users it amassed before LendUp, as first reported by Fintech Business Weekly, quietly entered liquidation. As part of that liquidation, it appeared that LendUp sold or transferred its neobank assets, including user accounts, to Kinly (formerly known as First Boulevard and Be Tenth) — though neither representatives for LendUp/Ahead nor Kinly ever responded to inquiries confirming this to be the case.

Users of Kinly, including those transferred from Ahead Money, have been complaining on social media and in app store reviews that, while they can deposit money to Kinly, they’ve been unable to transfer money out of the app, and have faced long delays in receiving debit cards or even getting responses from Kinly’s customer service team.

In fact, if you call Kinly’s customer service line today, you’ll still hear a message warning that the transfer funds feature is unavailable — which has been the case for months now.

Bancorp’s Response to a Consumer Complaint

I had opened and funded an Ahead Money account, which was subsequently transferred to Kinly without notification.

When I was unable to access the account, I reached out to the Kinly team via phone and email, and I was assured an agent would investigate and get back in touch with me within a day or two.

When I never received a response, I tried to imagine what an average user might do and filed a complaint with the CFPB on August 3rd. On August 25th, I received a notification the complaint had been forwarded to the FDIC — the primary federal regulator of Ahead/Kinly’s partner bank, The Bancorp Bank.

On September 13th, presumably after Bancorp was contacted by the FDIC, Kinly emailed me the following (emphasis added):

“Thank you for your email inquiry concerning your account. Please note, your account is active and your card is available for use to access your remaining balance.

Thank you for trusting us to service your financial business needs.”

A couple of days later, I received a letter from Bancorp, responding to the original forwarded CFPB complaint:

Several aspects of Bancorp’s response are notable, if not worrisome.

The letter confirms that my Ahead Money account was indeed transferred to Kinly (again, without opt-in permission or any notification)

Bancorp confirms Kinly closed the account — but, curiously, states this was “based on the detection of activity deemed to be high-risk.” If it were true, this might make sense — but, beyond the initial funding of the account (from a linked checking account in the same name), the account had zero transactions. It’s unclear if Bancorp itself conducted any investigation, or if it relied on and took at its word its fintech partner, Kinly.

Transaction history as displayed in the Kinly app on 9/24/2022 Bancorp’s letter correctly notes that I contacted Kinly on July 26th, though it incorrectly describes the agent as telling me that “Kinly had acquired the [Ahead Money] program.” Instead, an agent misleadingly told me that Ahead had “rebranded” to Kinly. Bancorp also falsely claims that Kinly instructed me to provide “specific identification documents” — at no time did a Kinly agent ask for nor did I provide any identification documents.

Finally, Bancorp claims Kinly reviewed identity documents and re-opened the account on August 3rd. However, I received no notification or communication from Kinly at that time. It wasn’t until September 13th — after Bancorp had received the complaint from the FDIC and presumably reached out to Kinly — that I received an email from Kinly customer support indicating my account was active.

Bancorp also sent the complaint response to the wrong address — the submitted complaint included the correct address in Illinois, whereas Bancorp’s response erroneously included the state as Michigan.

Bancorp Has a New Regulator: The OCC

Of course, we need to be careful about generalizing from a single anecdotal data point.

However, Bancorp has a history of inadequately supervising its partners. In fact, Bancorp was operating under a consent order with the FDIC until mid-2020 for problems that included “failing to provide promised protections to consumers in the resolution of account errors.”

Now that Bancorp has completed its transition to a national bank charter — just last week! — it is overseen by none other than the OCC.

Unlike the state regulators and FDIC to date, the OCC has recently shown a much stronger appetite to scrutinize “banking-as-a-service” arrangements and, if it finds problems, to take forceful action to correct them.

In addition to Kinly, Bancorp provides various banking services for other fintechs, including for SMB neobank NorthOne, Venmo and PayPal, and some of Chime’s 14.5 million users (some of whom have had complaints about abrupt account closures.)

Presumably, Bancorp went under the OCC’s microscope during the charter conversion process — but that doesn’t mean newly detected problems at its third-party partners couldn’t draw fresh scrutiny from its new regulator.

Representatives for The Bancorp Bank did not immediately respond to a request for comment prior to publication.

Starling Bank’s Bounce Back Loan Fraud

The UK, like other wealthy countries, rushed to support its economy as the potential disruption of the COVID pandemic became clear in early 2020. That April, the UK government announced its “Bounce Back Loan Scheme.”

While intended to fulfill a roughly comparable objective to the US’s Paycheck Protection Program (PPP), the structure of the Bounce Back Loan Scheme (BBLS) has some important differences.

With BBLS, the maximum amount businesses could qualify for was capped at £50,000 — PPP loans, on the other hand, were capped at 2.5x average monthly payroll expense, up to a maximum of $10 million.

Another key difference — the UK’s were designed to be paid back over a 6 or 10 year term after an initial 12 month grace period and carried a low 2.5% interest rate. The US PPP “loans” were intended to be forgiven.

Both the PPP and the BBLS were intermediated by private lenders with the US and UK governments, respectively, fully guaranteeing the loans. The government guarantees incentivized lenders to make the loans, as they captured the upside, while bearing none of the risk.

Perhaps unsurprisingly, the rapid roll outs of the programs and government backstop made the loans a ripe target for fraudsters. A 2021 analysis of the PPP program showed as many as 15% of the program’s loans could be fraudulent — with fintechs originating a disproportionate share of potentially bogus loans. The analysis of PPP loans found that while fintech lenders accounted for 29% of originations, they disbursed more than half of the program’s suspicious loans.

In the UK’s BBLS, the large majority of loans were originated by establishment banks like Barclays and HSBC. The only “fintech” (though it is a fully licensed bank) in the top 10 originators by volume is neobank Starling.

The approximately £1.6 billion that Starling originated as part of the BBLS helped it grow its loan book substantially. It also earned Starling around £36.2 million, according to recent analysis from Marc Ruby, helping the bank to report its first full year of pre-tax profitability for its financial year ending March 2022.

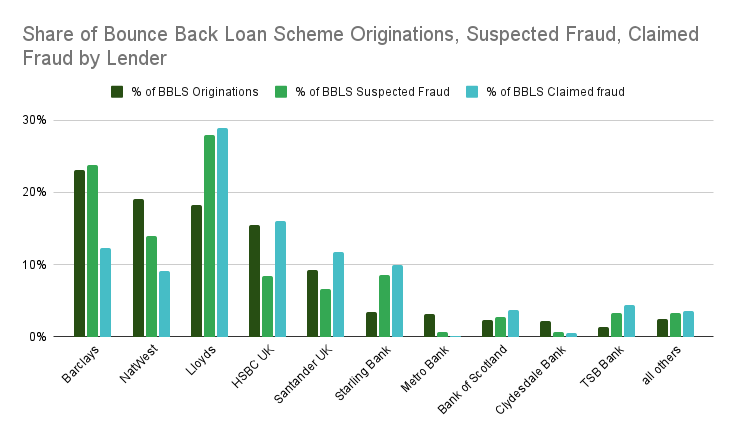

Based on recently released data on the BBLS, Starling’s suspected and claimed rates of fraud are substantially higher than many of its establishment bank peers.

While Starling accounted for just 3.44% of loan origination volume, it accounted for 8.5% of loans that are suspected to be fraudulent and 9.93% of guarantee claims made to the government on grounds the loan was fraudulent.

(h/t to Marc Ruby at Net Interest, which referenced this data set couple weeks ago)

Other Good Reads

Banking for Tomorrow Report (Fincog)

Three Years of Takes (Fintech Takes)

Three Steps to Diversify Your Network (WTFintech?)

Contact Fintech Business Weekly

Looking to work with me in any of the following areas? Email me.

Fintech advising & consulting

Sponsoring this newsletter

News tip or story suggestion

Early stage startup looking to raise equity or debt capital

Looking for Walmart Readies ONE & Citi to Exit UK Retail Market?

There’s more Fintech Business Weekly below for paying subscribers👇 — if you already subscribe, thank you for helping make this newsletter possible!