Amex-Backed TrueAccord Cited for Collecting on Illegal Tribal Loans

Varo Layoffs Extend Runway Just 9 Days, Starling Abandons EU License Ambitions, Goldman Earnings, Upstart Loses a Bank Partner, Bipartisan Stablecoin Bill Emerges

Hey all, it’s Jason.

Well, I survived the European heatwave! Temps here in the Netherlands did hit about 100° on Tuesday, before returning to a more normal rainy 70° by the end of the week.

Although it’s still peak summer, I’m already looking forward to (and making plans for) Money2020 this October. I’m working on a couple exciting things tied to the event — stay tuned for updates in coming weeks!

Existing subscriber? Please consider supporting this newsletter by upgrading to a paid subscription. New here? Subscribe to get Fintech Business Weekly each Sunday:

2022 Is A Whole Different World, Higher Risk Customers, Larger Investigations!

Sponsored content: Payoneer Selected ThetaRay's AI-powered SaaS AML transaction monitoring solution for its global business.

“We've had exposure to COVID, we've seen interest rate fluctuations, wars and conflicts have been happening, and we see further exposure to financial crime. Machine Learning and AI will enable us to adapt and respond to our models and risks much faster,” said Payoneer’s Chief Compliance Officer Micheal Sheehy.

Payoneer is the world's go-to partner for digital commerce everywhere. From borderless payments to boundless growth, Payoneer promises any business, in any market, the technology, connections, and confidence to participate and flourish in the new global economy. “We were super impressed when we went through our proof of concept with ThetaRay,” says Micheal Sheehy, My compliance department needs to be agile and quick to respond.”

TrueAccord Enters Connecticut Consent Order For Collecting on Illegal Tribal Loans

Digital debt collection startup TrueAccord, backed by marquee investors that include Nyca Partners and American Express, entered into a consent order with the Connecticut Department of Banking late last month to resolve charges it violated state law by collecting on small-dollar, high APR loans originated by lenders affiliated with federally recognized Native American tribes. (Full disclosure, TrueAccord has previously been a sponsor of this newsletter.)

The order stems from the result of a recent exam, which found TrueAccord collected on loans illegally originated to Connecticut borrowers by a tribal lender from January 2015 until at least November 2020. Per the consent order (emphasis added):

“[T]he Commissioner alleges that from January 2015 to June 2016, TrueAccord collected on loans made by lenders affiliated with federally recognized Native American tribes, unlicensed in Connecticut, that charged interest at a rate of greater than 12% per annum on loans in amounts of fifteen thousand dollars or less, in violation of Section 36a-573(a) of the Connecticut General Statutes, in effect at that time, and from July 2016 to at least November 2020, TrueAccord collected and received payments on small loans in amounts less than five thousand dollars made by lenders affiliated with federally recognized Native-American tribes, unlicensed in Connecticut, that had annual percentage rates of greater than 36%, in violation of subsections (b) and (c) of Section 36a-558 of the Connecticut General Statutes;”

A TrueAccord spokesperson confirmed the company has worked with tribal lenders, arguing it was be better for TrueAccord to serve these customers than another debt collection firm. In an emailed statement, the spokesperson explained:

“TrueAccord entered into a consent order with the Connecticut Department of Banking following a standard collection agency audit regarding lenders affiliated with federally-recognized Native American tribes. As a result, TrueAccord has stopped collecting on Connecticut accounts owed to lenders owned by Native American tribes and is refunding consumers who made payments on those accounts. TrueAccord did not admit or deny that any of our practices violated the Connecticut statutes. Instead TrueAccord entered into this Agreement and continues to focus on our mission to create better experiences for consumers in debt.”

In addition to the allegations of collecting on illegal loans, the consent order also resolves charges that TrueAccord commingled monies from its business accounts with those in its trust accounts and engaged in unfair or deceptive practices by advertising financial products of unlicensed affiliates.

Rent-A-Tribe Has Been Known Risk Since 2010s

So-called “rent-a-tribe” arrangements that are used to skirt state usury caps to offer high-interest, short-term loans exploded in popularity in the 2010s. But by the end of the decade, the bigger players in the space, including now-notorious Scott Tucker and Dallas-based Think Finance, faced numerous legal actions (TrueAccord’s consent order didn’t specify on behalf of what tribal-affiliated lenders it was collecting.)

Ultimately, multiple cases, including 2015’s Great Plains Lending, LLC v. Dep’t of Banking in the Connecticut Supreme Court and Gingras v. Think Finance, Inc. in the Second Circuit Court of Appeals found that sovereign immunity did not shield tribal officials for conduct taking place off the reservation that violates state laws. The FTC case against Tucker, originally filed in 2012, also brought increased scrutiny to the practices of tribal-affiliated lenders.

Ultimately, Think Finance restructured, spinning out brands RISE, Elastic, and Sunny into a new company, Elevate, which still operates today.

Think Finance itself descended into bankruptcy. Scott Tucker faced a $1.3 billion fine, which was ultimately dismissed, though he was sentenced to 16 years in prison; he was ordered to pay $40 million in back taxes in connection to the scheme as well as an additional three-year prison term (there’s a really great episode of Netflix’s Dirty Money series profiling the Scott Tucker saga.)

Could Collections Firms Be Targets in Fintech/Bank Partnerships?

In TrueAccord’s case, the actual number of impacted consumers seems to be quite small; according to the Department’s statement, 103 Connecticut borrowers would receive refunds totaling $44,000 as a result of the order.

A TrueAccord spokesperson confirmed that outcome, stating via email:

“TrueAccord has stopped collecting on Connecticut accounts owed to lenders owned by Native American tribes and is refunding consumers who made payments on those accounts. TrueAccord did not admit or deny that any of our practices violated the Connecticut statutes.”

What’s surprising is that TrueAccord was still working with tribal lenders as recently as November 2020, according to the Connecticut consent order, given the sector’s questionable reputation and practices that gave rise to numerous cases throughout the 2010s.

Presumably, whatever lenders TrueAccord was collecting on behalf of originated loans to consumers in other states — meaning the company could face similar scrutiny in other jurisdictions.

While the prominence of “rent-a-tribe” models has decreased significantly, disputes about so-called “rent-a-bank” arrangements continue to swirl.

Depending on the outcome of such cases, one can imagine a re-run of Connecticut’s argument in the TrueAccord case for third-party collectors servicing debts stemming from fintech/bank partnership arrangements where the terms of the loan would violate state usury law if the non-bank fintech is determined to be the “true lender,” though such an approach would mark a substantial escalation from today’s status quo.

Update 7/29/2022: Updated TrueAccord’s statement at the company’s request.

Varo’s Layoffs Extend Runway By Just Nine Days

Varo, the first US neobank to win a de novo charter, has laid off about 10% of its staff in a bid to extend its runway. As first reported here in Fintech Business Weekly, the fledgling bank was on track to run out of cash by the end of this year, based on its net loss and equity capital reported in its first quarter call report.

At that time, just six weeks ago, the most likely path forward seemed to be a combination of layoffs and reduced marketing spend to extend the company’s runway, giving it a chance to improve its economics and seek additional funding.

At the time, Varo CEO Colin Walsh told Banking Dive, “We remain very well capitalized and have sufficient capital to reach profitability, without having to raise additional capital.”

While Walsh reiterated his claim that Varo has sufficient capital to execute on its strategy, his blog post last week explicitly linked the layoffs and reduced marketing to the need to extend the company’s runway (emphasis added):

“As a business, we are not immune to the impacts of our current environment and we must make some difficult decisions to ensure that Varo has sufficient capital to execute on our strategy and path to profitability. This is in addition to steps we’ve taken to decrease our burn rate, including limiting hiring to the most critical roles and pulling back on marketing investments in the near-term.”

Based on average employee annual compensation of $132,586 in 2021, laying off 75 employees will save Varo about $10 million per year, though there will be costs associated with the restructure.

The savings (assuming no severance or restructuring costs) would only extend Varo’s runway by about nine days.

The far bigger lever for Varo is marketing expense — something the company spent a whopping $38.6 million on in the first quarter of 2022, or $154.4 million on an annualized basis.

While it is likely faster and easier to reduce marketing spend than conduct layoffs, doing so virtually guarantees slower growth. It’s unclear how sticky Varo’s customers are, but if data from MoneyLion and Dave, which serve similar users, are any indication, Varo could face high user churn.

With the significant fixed expenses of operating as a bank, slower growth and potentially high churn means fewer accounts over which to spread those costs.

Varo can try to grow revenue from its existing customers — the average revenue per account is a paltry $24 per year, based on Q1 filings. But that may be an uphill battle in a deteriorating economic climate and given the consumer segment Varo serves.

What is “Varo Tech”?

Beyond the layoff announcement, Walsh mentioned a reorganization and the creation of a new business unit, dubbed “Varo Tech.” Per the post (emphasis added):

“As part of this transition, we will be establishing a new business unit, Varo Tech, which will bring together the Technology, Design, Data and Product functions under a single umbrella. This new structure will allow us to increase pace, reduce costs, and, as always, ensure our focus remains on technology innovation and continuing to engage and grow our customer base. It also enables us to reduce silos across the company and drive more cross-functional collaboration.”

It’s unclear if the restructure portends a new business line or change in focus. The naming suggests a B2B rather than consumer focus.

Varo wouldn’t be the first consumer fintech to attempt to monetize something built for the consumer market — credit card startup Petal offers its cashflow underwriting tech under the name Prism Data; consumer lending company Avant spun out its homegrown tech stack as a standalone software company, Amount.

Unlike those companies, Varo holds a prized position: its banking license. One could imagine Varo following in the path of licensed UK neobank Starling, which expanded from consumer and SMB banking to offer banking-as-a-service.

Still, Varo’s position as a newly launched regulated bank may make such pivots more difficult, as its primary regulator, the OCC, would likely need to review and approve material changes to its business plan.

Goldman Earnings: Profit Drops 47%, But Consumer Unit Shines

It’s earnings season, and that means it’s time for my quick spin through Goldman’s report.

While much of the press coverage focused on the firm’s drop in revenue (down 23% vs. Q2 2021) and net earnings (down 47%), consumer banking (Marcus) saw revenue jump 67% vs. Q2 2021, powered by higher deposit and credit card balances, according to the firm — though a chunk of those card balances, reportedly some $3 billion, came via the acquisition of the GM co-brand portfolio from Capital One.

More details and analysis in a brief tweet thread from last week —

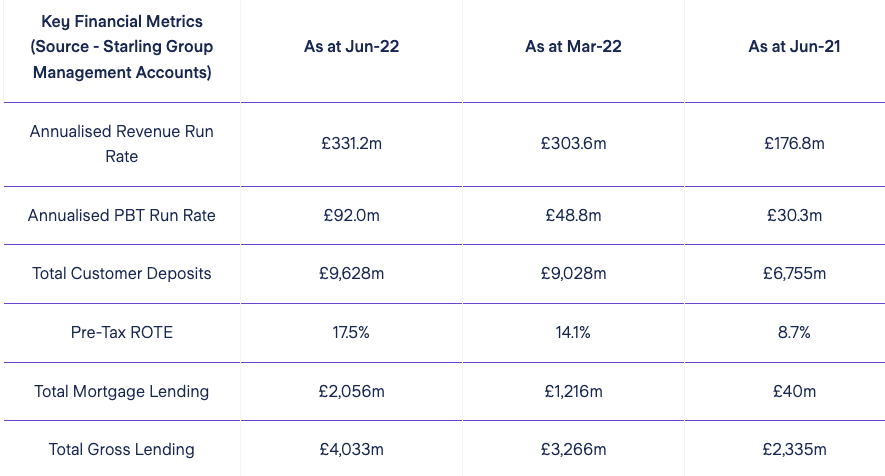

UK Neobank Starling Turns a Profit, Abandons EU License Ambitions

It was a mixed bag for UK neobank Starling last week.

The bank has taken a notably different path than fellow UK startups Monzo and Revolut. Starling has opted for slower growth, a focus on its home market of the UK, and building a loan book, whereas Revolut and Monzo have largely eschewed lending.

Starling’s efforts to build its loan book were substantially boosted by its participation in the UK’s Business Bounce Back Loan Scheme (somewhat comparable to the US’ PPP loans). Facilitating the loans helped Starling grow its loan book from nearly zero in 2019 to approaching £2.2 billion in 2021.

Starling also got into mortgage lending through its acquisition of Fleet Mortgages for £50 million last July. As of this June, the bank held some £2 billion in mortgages on its balance sheet.

Starling’s focus on growing lending helped power its first full year of pre-tax profitability.

Still, it wasn’t all good news for the bank last week.

After a lengthy four-year process during which it faced multiple setbacks, Starling has withdrawn its application for an EU banking license from the Irish central bank. The license would have facilitated Starling’s expansion into EU countries.

Instead, Starling plans to refocus on expanding its lending in the UK and selling its homegrown software to other banks to assist with their “digital transformation” strategies.

FT Partners: Q2 Report Shows Fintech Funding Trending Toward Pre-Pandemic Levels

As public market valuation corrections have continued washing through to private fintechs, it’s worth paying attention to the VC ecosystem to get a sense of where things are going.

US venture capital firms raised $121.5 billion in the first half of 2022, a significant jump from the $74.1 billion raised during the same period in 2021, leading many to talk about a glut of “dry powder.”

But it’s not like that $121.5 billion represents cash sitting in VC firms’ bank accounts; rather, it represents capital commitments made by their LPs — as VCs source and make investments, they call on their LPs to actually post the funds to fulfill those promises.

So despite the appearance of VCs sitting on piles of cash, firms may be facing pressure from their LPs to slow their roll, so to speak, as players throughout the ecosystem wait to see how the current economic turmoil plays out.

Against that backdrop, it shouldn’t be surprising to see fintech deal volume continue to shrink — especially as the IPO “window” has slammed shut. This is clearly reflected in FT Partner’s latest Quarterly Insights report.

Looking specifically at fintech (excluding crypto and blockchain companies), monthly financing volume is trending back towards 2020 levels.

Considering the abrupt re-focus from “growth at all costs” to profitability, it’s actually somewhat remarkable funding levels remain as high as they are, though there has been a pullback from larger, late-stage rounds in favor of earlier stage companies, many of which may be pre-revenue or even pre-product.

Other Good Reads

Don’t Spend Your Crypto With A Coinbase Debit Card (Ron Shevlin/Forbes)

FTX pitches plan to get Voyager customers some of their money (Protocol)

Buyer Beware: Community Bank Equity At Risk (Something Clever)

Contact Fintech Business Weekly

Looking to work with me in any of the following areas? Email me.

Sponsoring this newsletter

Content collaboration or guest posting

News tip or story suggestion

Early stage startup looking to raise equity or debt capital

Looking for “Upstart Loses a Bank Partner” and “A Bipartisan Stablecoin Bill Emerges”?

There’s more Fintech Business Weekly below for paying subscribers👇 — if you already subscribe, thank you for helping make this newsletter possible