GENIUS Passed Into Law. Now What?

California Regulator Appears to be Investigating Synapse-Linked Fintech, CFPB Seemingly Surprised Chase Wants to Charge For Banking Data

Hey all, Jason here.

We’re firmly into the middle of summer, and apart from (hopefully) warm weather and barbecues, that means one thing: vacation season.

Sadly, I don’t have a proper summer vacation scheduled, but my better half’s family is visiting the first half of this week here in the Netherlands, and we’ll all head together to Paris later this week. If you have any can’t-miss food suggestions for the City of Lights, let me know!

This API Is Reshaping Consumer Credit

Sponsored by Spinwheel: Why is consumer debt management so antiquated? Why rely on processes that add friction and costs when the tech to streamline it is already here?

Imagine unlocking key financial details instantly — with just a phone number and birthdate. That’s what Spinwheel does.

Spinwheel flips the script on consumer credit and payments. Their Debt APIs give brands real-time, verified data and seamless payment processing — without customers leaving their ecosystem.

GENIUS Passed Into Law. Now What?

On Friday, President Trump capped off “Crypto Week” by signing the GENIUS Act into law, describing it as an “exciting new frontier.”

The measure creates a dual federal and state licensing and oversight framework for “payment stablecoins,” which are defined as:

a digital asset that is, or is designed to be, used as a means of payment or settlement;

and the issuer of which is obligated to convert, redeem, or repurchase for a fixed amount of monetary value, not including a digital asset denominated in a fixed amount of monetary value;

and represents that such issuer will maintain, or create the reasonable expectation that it will maintain, a stable value relative to the value of a fixed amount of monetary value.

Payment stablecoins are not FDIC-insured and issuers cannot pay yield (interest) on them — though GENIUS doesn’t prohibit other entities, like crypto exchanges, from paying yield (more on why this is a critical distinction later…)

GENIUS specifies that payment stablecoins are not:

national currency;

a deposit, as defined by the Federal Deposit Insurance Act (including a deposit recorded using distributed ledger technology);

or a security, as defined in the Securities Act of 1933, the Securities Exchange Act of 1934, or the Investment Company Act of 1940.

GENIUS lays out three categories of “permitted payment stablecoin issuers,” or PPSIs:

insured depository institutions, via a subsidiary that applies and is approved to issue stablecoins by their relevant federal regulator (eg, the Federal Reserve, the OCC, or the FDIC);

nonbanks, uninsured national banks (such as the national trust banks that existing stablecoin issuers Circle and Ripple have applied to charter), and federal branches of foreign banks, by applying to and receiving approval from the OCC;

nonbanks that issue an aggregate of less than $10 billion in stablecoins can opt to apply to their relevant state stablecoin regulator.

It’s worth noting that individual states are not required to create their own licensing and regulatory regimes, but, if they do, they are required to do so in the same one-year period defined in the law for federal regulators to develop implementing rules.

GENIUS creates a new body, the Stablecoin Certification Review Committee, which is composed of the Secretary of the Treasury, the Chair of the Federal Reserve, and the Chair of the FDIC.

The Stablecoin Certification Review Committee is tasked with:

reviewing and approving or denying certification that a state’s regulatory regime is “substantially similar” to the federal framework, which the committee must do within 30 days of receiving a submission;

overseeing issuers’ transition from state to federal regulatory regimes, for entities that opt to be state-licensed but grow to exceed the $10 billion threshold;

formulating, in conjunction with other relevant regulators, rules and standards, capital requirements, and operational protocols;

and reviewing and approving or denying stablecoin issuer applications from companies that are not primarily engaged in financial services.

The last element is worth highlighting, as it means if a non-financial services firm — think big tech, like Google or Apple, or major retailers, like Walmart and Amazon — sought to issue their own stablecoins, the SCRC would need to unanimously sign off on their application to do so.

Consistent with the definitions laid out above, the Securities and Exchange Commission, the Commodity Futures Trading Commission, and the Consumer Financial Protection Bureau have no role to play in the licensing or supervision of PPSIs.

GENIUS seeks to ensure issuers’ ability to redeem stablecoins for fiat USD by permitting a relatively limited set of reserve assets that include:

US cash and currency

balances held at a Federal Reserve Bank

funds held as demand deposits at insured depository institutions

short-term US Treasury bills, notes, or bonds with a remaining maturity or original maturity of 93 days or fewer

overnight repurchase agreements backed by short-term Treasuries

reverse repurchase agreements backed by Treasuries (with specific terms and counterparty requirements)

securities issued by a registered investment company or government money market fund that invest solely in the above listed assets

other similarly liquid US-government issued assets, if approved by a stablecoin issuer’s primary regulator

tokenized versions of any of the above, except for repurchase agreements and reverse repurchase agreements

GENIUS further calls for entities that provide custody or safekeeping services for the reserves backing stablecoins to:

segregate customer assets from proprietary assets;

be subject to appropriate regulatory oversight;

submit relevant operational and asset protection information;

treat customer assets as customer property;

in the event of bankruptcy, give customer claims priority over custodian creditors for backing assets held in custody.

Stablecoin issuers are generally prohibited from reusing, pledging, or rehypothecating reserve assets.

Issuers must publish detailed monthly reports of reserve assets that are certified by company executives and undergo a monthly third-party audit of reserves. Issuers with more than $50 billion in outstanding stablecoins, even if not publicly traded, must prepare annual audited financial statements that are filed with regulators and are publicly available.

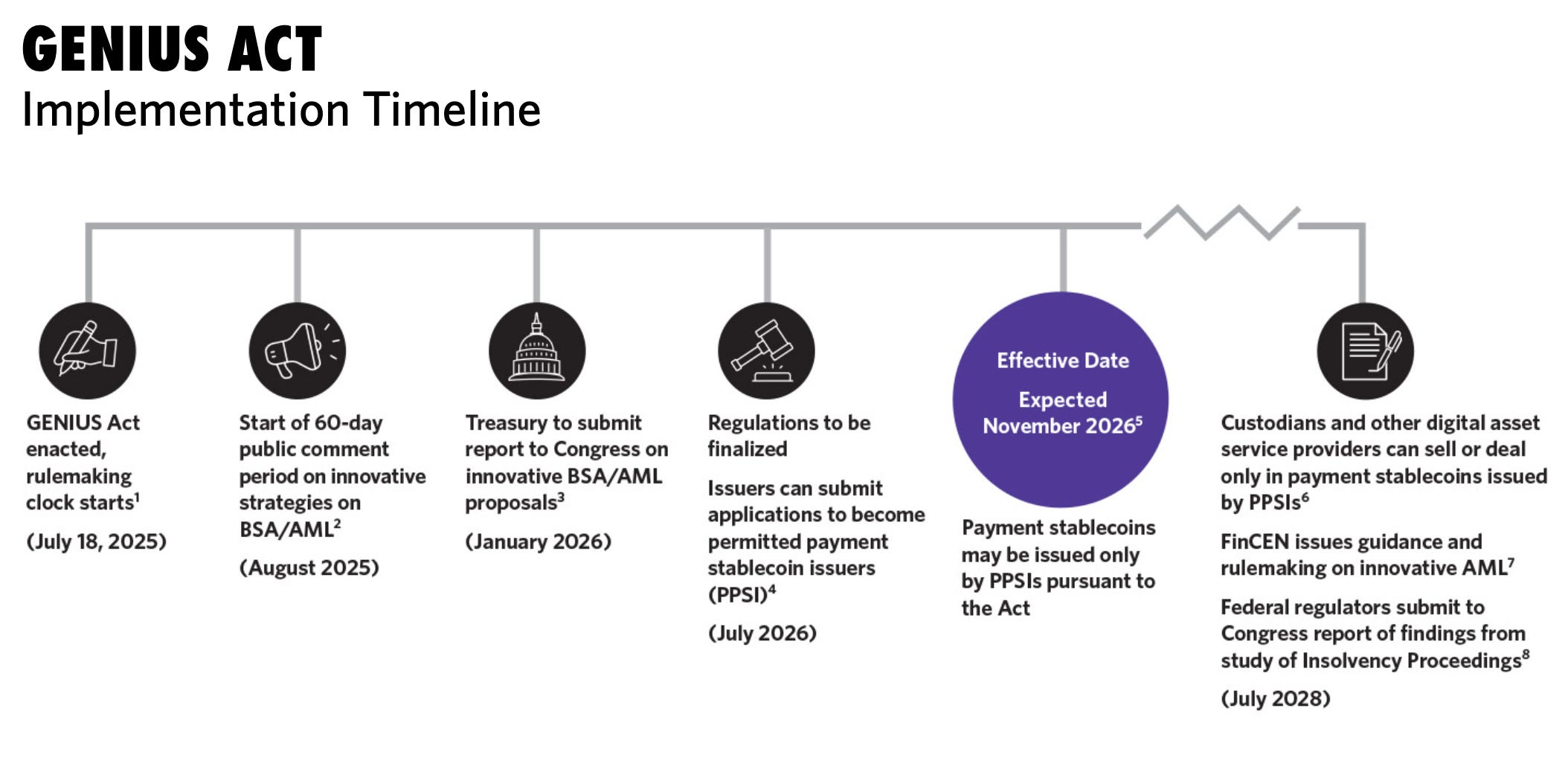

Trump’s signature on GENIUS passes it into law, kicking off an implementation period that will take 18 months or until 120 days after the date on which primary federal stablecoin regulators issue any final implementation regulations, whichever comes first.

It is expected that GENIUS will become effective around November 2026.

There is a three year “grace period” from the passage of GENIUS for existing stablecoin issuers to become licensed and come into compliance with the law, meaning that in July 2028, it will become unlawful for US digital asset service providers to offer or sell payment stablecoins to a person in the United States from an unlicensed issuer.

How Might GENIUS and Stablecoins Reshape Banking, Payments, And The Wider Global Economy?

Perhaps the biggest and most immediate impact of passing GENIUS is something the wider crypto industry has been seeking for a long time: certainty (though the CLARITY Act, which would define market structure for cryptocurrencies, as opposed to stablecoins, passed the House last week, it has yet to pass the Senate.)

With an implementation window expected to run through November 2026 and a grace period for existing stablecoins through July 2028, the impact on stakeholders is likely to be more evolution than revolution.

With that caveat that what follows is more “thinking out loud” than firmly held points of view, this is how I see the continued growth of stablecoins impacting various stakeholders in the medium to long term.

US Treasury: with the relatively strict definition of permissible reserve assets, the US Treasury is likely to see an increase in demand for Treasuries — and that demand will be price inelastic, as issuers are likely to need to purchase Treasuries as reserve assets as a function of market demand for their stablecoin, regardless of what Treasuries yield at given point in time.

Indeed, policymakers have explicitly touted this as a potential benefit of passing GENIUS, with Treasury Secretary Bessent predicting stablecoin issuance could generate as much as $2 trillion in demand for Treasury debt in the next few years.

Demand from stablecoin issuers is also expected to modestly decrease yields, making it less expensive for the US Government to borrow money.

While this is understandably viewed as a positive by some, it doesn’t come without risks — specifically, the impact of a potential “run” on a stablecoin causing disruptions in the Treasury markets.

Given the constraints on the duration of Treasuries eligible to be held as reserve assets, there is also the potential risk of distortion to the yield curve from price insensitive demand from stablecoin issuers for assets of specific durations.

US foreign policy: the potential impacts across US foreign policy are extensive, but perhaps the most likely and relevant is as an antidote to the declining dominance of US dollar hegemony.

While, as the saying goes, rumors of the dollar’s demise have been greatly exaggerated, it is true that as the US has leaned more heavily on financial tools, like sanctions, to conduct foreign policy, it has given other countries, especially geopolitical rivals, motivations to reduce their dependence on the US dollar and Western financial systems.

One of the primary use cases for stablecoins — specifically USD-pegged stablecoins — is for the preservation of purchasing power for those that live in countries with unstable currencies, high levels of inflation, or the risk of government appropriation of private assets.

While Americans were understandably frustrated when inflation hit 9% during the COVID-19 pandemic, in many countries, double-digit inflation is the norm, not the exception, with extreme cases like Venezuela and South Sudan seeing annual price increases of over 100%.

Historically, it has been difficult to access US dollars in some countries, particularly those with unstable economies or currencies, foreign exchange and capital controls, and high inflation.

Even in countries without such challenges, the ability to save and invest in US dollars is often limited to the wealthy. Stablecoins are posed to actually make good on the promise of “democratizing” access to dollars, even for those at the lower end of the income and wealth spectrum.

Putting these synthetic US dollars in the hands of retail users around the world is likely to become a potent geopolitical tool that could be deployed in a variety of ways, ranging from a form of soft power through to more coercive tactics comparable to traditional financial system tactics of sanctions or the financial “death penalty” of being banned from Swift.

Foreign governments and banks: the logical counterpoint to the geopolitical benefits that may accrue to the United States are the risks and challenges other governments may face if their populations adopt USD-backed stablecoins at a material scale.

A country’s widespread adoption of stablecoins would effectively drive capital out of the country and into the US in the form of growing reserve assets backing those stablecoins, most likely Treasuries. Functionally, foreign holders of USD-linked stablecoins would be financing the US Government’s budget deficit.

Growing dollarization would also undermine the efficacy of countries’ monetary policy and risk disintermediating local banks by reducing deposits and liquidity, with knock-on impacts in their ability to lend to local populations.

US banking regulators: the passage of GENIUS, by definition, means an increased workload for federal bank regulators, who must formulate regulations to implement the law, adjudicate license applications, and oversee stablecoin issuers, including for BSA/AML compliance — all as the Trump administration has pushed to cull the government workforce, including at these very regulatory agencies.

But regulators will also be tasked with monitoring the impact of a growing volume of stablecoins on the existing banking system and the real economy. Some analysts have expressed concerns that stablecoins will drain deposits from the banking system, reducing banks’ ability to lend and potentially interfering with the transmission of monetary policy.

In theory, policymakers addressed this risk by prohibiting stablecoin issuers from paying interest, making it expensive for users to hold funds as stablecoins vs. as traditional interest-bearing bank deposits.

But while GENIUS prohibits issuers from paying interest or other material consideration, it doesn’t block other entities from doing so.

For example, Coinbase, which was a cocreator of USDC, receives 100% of the interest generated from the reserve assets underlying USDC held on its exchange and 50% of the interest generated from USDC held elsewhere.

Coinbase, in turn, passes along a portion of this to users holding USDC on its platform as a “reward.”

There’s also the matter of the increased potential for disruption in crypto markets to be transmitted into the traditional banking system via stablecoins and their backing assets.

A rapid wave of stablecoin redemptions would force a stablecoin issuer to draw down its reserve assets, whether liquid bank deposits or by selling Treasuries. At a significant enough scale, this could case liquidity challenges to banks holding deposits as reserves for issuers or cause a drop in Treasury prices.

This isn’t purely theoretical. The “crypto winter” of 2022 is widely understood to have led to the voluntary liquidation of Silvergate Bank. And, at the time when Silicon Valley Bank failed a few days later, it $3.3 billion in deposits as reserve assets for stablecoin issuer Circle. This amounted to about 8% of the assets backing Circle’s USDC stablecoin.

The situation caused a panic that Circle might not be able to redeem USDC at par, leading to USDC “breaking its peg” and briefly trading as low as $0.876.

Stablecoin issuers: there are more than 200 USD-pegged stablecoins in circulation, worth an aggregate of about $260 billion in value.

By comparison, all USD-pegged stablecoins amount to about 1% of the $22 trillion of M2 money supply, a broad measure of the money supply that includes currency and various sorts of bank and money market mutual fund deposits that are relatively liquid.

Apart from Tether (USDT), which accounts for about 62% of all USD stablecoins in circulation, with approximately $162 billion issued, and Circle (USDC), whose $64 billion in circulation gives it about a 25% market share, most stablecoins amount to a rounding error.

Even Trump-linked World Liberty Financial’s USD1, the seventh most popular USD-pegged stablecoin, has a market share of less than 1%. PayPal’s PYUSD, launched with great fanfare in August 2023, has less than $1 billion in circulation nearly two years later.

Stablecoin issuing as a business is perhaps the ultimate scale game: hold Treasuries, issue tokens, and collect the interest. This seems likely to become even more the case with an emerging regulatory regime that issuers that want to operate in the US market will need to adhere to.

The economics of issuing stablecoins is inherently extremely sensitive to the interest rate environment.

While issuers have profited handsomely in recent years, with the Fed poised to reduce rates as it shifts its focus from inflation and price stability to maintaining full employment, stablecoin issuers are likely to see their business model negatively impacted.

It seems incredibly unlikely that 200+ issuers, particularly ones with little circulation, will have the capacity and interest in navigating the US licensing process and being bound by the relevant rules and regulations.

Instead, what seems more likely to happen is a bifurcation between US licensed issuers — an “onshore” market — and those that eschew licensing and forgo being officially sanctioned for use in the US — an “offshore” market.

Interestingly enough, Paolo Ardoino, the CEO of Tether, which has historically had a mixed reputation, insists that the issuer will comply with GENIUS (I interviewed Ardoino back in 2022, including comments from him on why Tether doesn’t face the same risks that led to TerraLuna’s collapse, here.)

Tether has said it will pursue a dual-track strategy, launching a new US-based stablecoin designed to compete with Circle’s USDC, while simultaneously pursuing licensing as a foreign issuer for its existing USDT stablecoin within the three-year grace period.

Two US-based stablecoin issuers, Circle and Ripple, have already filed applications to charter national trust banks, which, if granted, would ease the path to being licensed as a stablecoin issuer, while also allowing them to custody their own reserve assets.

Big banks: at this point, it’s difficult to game out the overall impact on large banks like JPMorgan Chase, Citi, and Bank of America. Banks have an incredibly poor track record of self-disrupting, particularly if it means threatening existing, highly profitable lines of business.

But large banks are also quite capable of leveraging their existing distribution and market power to blunt competitive threats when they emerge and gain sufficient market traction.

Alex Johnson at Fintech Takes has written multiple pieces about how big banks have leveraged consortiums: entities like The Clearing House (ACH, RTP) and Early Warning Services (fraud data, Zelle).

Akoya, an open banking infrastructure company intended to disrupt the threat posed by firms like Plaid and MX, was spun out of Fidelity and is now jointly owned by firms that include Bank of America, Capital One, and JPMorgan Chase.

Recognizing the potential threat from stablecoins, it has been reported that major banks are exploring the idea of a consortium to issue a joint stablecoin.

While a stablecoin consortium could enable better interoperability of bank-issued stablecoins, major firms aren’t sitting on the sidelines: JPMorgan Chase launched its own JPM Coin, an institutional settlement token used on the bank’s permissioned blockchain, Onyx, in 2019.

More recently, the bank announced plans to develop a tokenized deposit, JPMD, which would act as a digital representation of traditional commercial bank deposits on Coinbase’s Base public blockchain.

And Citibank CEO Jane Fraser mentioned on the bank’s recent earnings call that it is also evaluating applications for stablecoins or tokenized deposits.

While the largest banks do face the risk of deposit flight described above, they also have the potential to benefit from holding the reserve assets, including deposits, of non-bank stablecoin issuers.

Larger banks are better positioned to hold the deposits or other reserve assets vs. smaller banks, as a stablecoin issuer of any significant volume could quickly become a concentration risk for a bank with a smaller balance sheet.

Small banks: smaller banks face the same risk of deposit flight without the potential silver lining of serving as custodian for issuers’ reserve assets. In what is already an incredibly challenging market for smaller institutions, stablecoins have the potential to become yet another competitive threat that smaller institutions are poorly armed to deal with.

Perhaps the most practical role smaller banks can play is as a bridge between “fiat” and stablecoin ecosystems; “on” and “off” ramps, in industry parlance. But even that role for smaller institutions may be unnecessary, if stablecoin issuers secure their own charters, enabling them to access traditional payment rails without relying on a third-party bank to do so.

Payment networks, remittance firms: some argue that stablecoins pose a serious competitive threat to incumbent payment rails, particularly older/slower/more manual rails (ACH, wires) or more expensive rails (card payments).

But history suggests that that is not the most likely outcome, at least for domestic payments use cases.

Apart from physical checks, the volume of various types of non-cash payments have increased over time — despite the introduction of new methods, like peer-to-peer payment apps, real-time payments, and crypto.

I find it rather unlikely that stablecoins will be a user-facing technology or rail in domestic payments use cases (but I could be totally wrong about this!)

On the other hand, cross-border payments and foreign exchange, handled through Swift and correspondent banking networks, are ripe for disruption.

Cross-border payments, particularly those involving “exotics” (low volume currency pairs) continue to be slow, expensive, and opaque.

Services like Sling Money replace Swift and correspondent banking networks with stablecoin rails and local country on- and off-ramping, making transactions faster and often less expensive than traditional cross-border payments.

Banks’ international payments and foreign exchange businesses, traditional remittance providers like Western Union and Moneygram, and fintech remittance services like Wise and Remitly may have the most to lose from growing use of stablecoins.

Indeed, stablecoin-powered remittances, card issuing and payments, and treasury management are already making inroads, particularly in countries and currencies where cross-border payments have remained stubbornly slow and expensive.

Crypto exchanges: it’s hard to argue that the clarity that GENIUS brings to the stablecoin space will be anything but a positive for crypto exchanges, particularly Coinbase, which has a direct financial stake in USDC’s success.

Crypto proponents are also hoping the passage of GENIUS paves the way for the CLARITY Act, generally viewed favorably by the industry, to pass the Senate.

One clear negative would be the requirement for US-based exchanges to delist stablecoins from issuers who do not comply with GENIUS and become licensed by the end of the three-year grace period.

While Tether has full throatedly said it intends to comply with GENIUS, if it decided not to or is unable to do so, it could be a significant blow to US exchanges forced to delist it.

Consumers: while some mainstream publications have described GENIUS “unlock[ing] cheaper, faster money for everyone,” it’s less clear to me that the continued growth of stablecoins is an unalloyed positive for consumers.

Requiring licensing, regulating permissible reserve assets, and mandatory disclosures and audits are surely an improvement from the wild west-like attitude that has reigned to date.

But the explosion in the number of USD-pegged stablecoins and the various, often incompatible blockchains on which they operate risk creating an increasingly fragmented, confusing landscape for consumers to navigate.

And while GENIUS will apply to stablecoin issuers that want their coins to be available in the United States, “offshore” issuing seems likely to remain largely unregulated for the foreseeable future.

While firms that offer these offshore stablecoins will likely need to make a good-faith effort to block American users via geo-filtering and KYC processes, getting around these restrictions can be as easy as turning a VPN.

But the consumers who are likely to be at greatest risk will be those who live outside of the United States and who may be poorly positioned to parse the differences between GENIUS-compliant issuers and those who are not — especially if they are being promised too good to be true benefits, like outsized interest rates.

For example, Ugly Cash, targeted largely at users in Latin America but describing itself as “America’s Stablecoin App,” converts users’ deposits to eUSD — and offers “rewards” on users’ balance of up to 8% APY.

A disclosure in the app notes that “the acronym ‘USD,’ as well as the symbol ‘$’ are used and displayed on various screens of this application as a reference to represent the value of a virtual asset called eUSD, not a balance in US dollars, even if it not referenced explicitly.”

But what is eUSD? The “decentralized, community-governed, censorship-resistant stablecoin,” with just $26 million in circulation, is backed by derivatives of Tether’s USDT and Circle’s USDC held in yield-generating defi protocols Aave and Compound.

Somehow, I suspect, many users of the app may not understand that they don’t hold dollars, but rather hold eUSD, which is a claim on a basket of aUSDC, cUSDC, aUSDT, cUSDT, which in turn are claims on USDC and USDT, which in turn are claims on those issuers’ reserve assets.

CFPB Official Seemingly Surprised Chase Wants to Charge for Banking Data; PNC’s CEO Suggests It May Follow Suit

On Friday, Bloomberg’s Evan Weinberger reported that at least one Trump-appointed official at the Consumer Financial Protection Bureau has raised concerns about reports that JPMorgan Chase intends to begin charging open banking firms and fintechs to facilitate consumers’ access to their own data.