Six Factors Changing BNPL in 2022; What's Wrong with Dave?

Drive Now, Pay Later's Slippery Slope, Apple Acquires Credit Kudos

Hey all, Jason here.

Spring has definitely sprung here in the Netherlands. Around the time this hits your inbox, I should be cycling through the tulip fields near Keukenhof — a favorite springtime activity here.

Existing subscriber? Please consider supporting this newsletter by upgrading to a paid subscription. New here? Subscribe to get Fintech Business Weekly each Sunday:

New York City’s Largest Fintech Event Returns This Spring

Sponsored content: On May 25th - 26th, LendIt Fintech USA returns to the Javits Center for 2 days of world-class content and long awaited face-to-face networking. Explore the complexities of today’s financial services industry through insightful sessions focused on the most important trends in banking and lending. Key topics include digital banking, Web3, green fintech, consumer lending, embedded finance and much more.

Save 15% on your pass with the code MEDIA15_FBW — see you there!

Top 6 Factors Changing BNPL in 2022

If buy now, pay later hit what felt like an uncontrolled growth spurt in 2021, perhaps 2022 is the year it matures. A confluence of factors will shape how the industry changes this year.

Regulation

Regulation is definitely top of mind this year, particularly after the CFPB opened an inquiry into the sector at the end of 2021. Areas the CFPB’s order highlighted as concerns include the risk of consumers accumulating debt, regulatory arbitrage, and “data harvesting” (a recurring theme for the CFPB.)

Looking at the questions the CFPB is asking BNPL firms, the CFPB is gathered data about how frequently consumers use BNPL (repeat use), for what amounts, category of purchase, repayment method, underwriting, late fees, and loan performance, among other topics.

Potential rule making seems likely to focus on consumers’ ability to pay, consumer protections (including disclosures), fees, and data collection and sharing.

The biggest risk from any new requirements is the potential introduction of additional friction into the experience. Collecting data to better assess ability to pay and providing additional consumer disclosures risks eroding one of BNPL’s key selling points: frictionless ease of use.

However, any rule making stemming from the market monitoring exercise would take months, if not years, to actually be implemented — though, as seen in the small-dollar industry, even the threat of rule making can drive significant changes in the market.

Credit Reporting

Another area destined to impact BNPL in 2022: credit reporting. The big three bureaus are already developing plans to enable BNPL providers to furnish their data. Approaches to incorporating this data vary. Equifax will add BNPL data to consumers’ main credit reports, while TransUnion and Experian will house this data separately from primary reports.

How might credit reporting impact BNPL providers? The obvious first order impact is that they must develop policies and procedures to ensure data they furnish is accurate and processes for investigating consumer disputes about data appearing on their reports, as required by the Fair Credit Reporting Act.

The second order impacts, however, may be more significant. Presently, a user’s split pay BNPL debt is invisible to potential lenders. As this data is added to the bureaus, BNPL providers will logically be under pressure to incorporate it in their underwriting. Combined with greater scrutiny of how BNPLs evaluate consumers’ ability to pay, this could result in consumers being approved for lower amounts or declined outright.

Rising Interest Rates

In the face of persistent inflation — now further exacerbated by Russia’s invasion of Ukraine — the Fed has taken a hawkish turn. The Fed has already raised rates by a quarter point and has made clear more, faster rate increases are on the table. The fed funds rate is expected to reach 2.25% by the end of year.

How might rising interest rates impact BNPL? Companies offering longer-term, interest-bearing financing, like Affirm’s core product, have more flexibility to pass along rising rates to borrowers.

Still, increasing rates should logically decrease demand for borrowing. Higher rates mean higher monthly payments and thus suggest lower approval rates. At the margin, bound by a 36% APR cap (and lower in some states), this could mean some consumers who were borrowing at the upper end of Affirm’s interest rates are no longer able to do so. Increasing rates also make 0% financing, popularized by Affirm’s partnership with Peloton, more costly for Affirm to offer.

And there are some early signs of stress in the securitization market, one way non-bank lenders access capital for longer term loans like the ones Affirm makes. Affirm recently canceled an ABS offering due to ‘market volatility.’ If borrowers begin to have trouble making payments and defaults exceed forecasts, a 2016-like scenario is possible, which saw ABS investors pull back from online lenders, forcing many to throttle originations.

BNPL providers offering split pay products will face rising rates on their debt facilities with fewer options to pass the increased cost along. A key feature of split pay products for the consumers is that they’re interest-free. Merchants foot the bill, via the merchant discount rate, but the amount merchants are willing to pay has been coming down as competition in the space has increased.

BNPL providers could try to make up for higher rates by getting creative with fees — but doing so risks running afoul of consumer advocates and regulators. Instead, BNPL companies may have to eat higher interest expenses and see their margins suffer for it.

Banks offering interest-bearing or split pay BNPL products are the best positioned to respond to increased rates — and, indeed, could even benefit. As banks still have a glut of deposits from pandemic-era stimulus and savings, most are in no rush to increase the rates they pay on deposits. This gives many banks a cheap source of deposits to fund BNPL offerings, while rising rates lets them charge borrowers more for longer-term interest-bearing BNPL plans.

Declining Merchant Discount Rates

The merchant discount rate is the percent of a transaction a merchants pays to the BNPL for providing split pay financing to their end customer. When BNPL was first becoming popular, this could reach as high as 7% of the transaction size.

As the BNPL space has become more crowded, the MDR has declined. PayPal charges merchants the same whether it’s processing a regular credit or debit transaction or a split pay plan: 3.49% + $0.49.

Presumably, larger merchants, like Amazon or Walmart, are able to negotiate even lower pricing.

The bottom line is the rate BNPL providers are able to charge merchants has declined, and that is unlikely to reverse.

Consolidation

As BNPL enters a more mature phase, there are a couple of common strategies to continue growing: moving ‘up funnel’ (shopping app, browser extension); offering a physical payment card; geographic expansion; and acquisitions.

Achieving geographic expansion, growing merchant footprint, and adding BNPL capabilities to an existing stack through acquisitions has contributed to a wave of consolidation in the sector:

Given the challenges ahead and general lack of differentiation between many players, more consolidation in the space is likely.

Potential for Increasing Losses

Split pay BNPL is a new and untested form of consumer debt. It’s unclear how it will perform through the credit cycle — though, as rates rise, we may find out.

Many consumers who use BNPL do so in addition to other forms of consumer debt, like credit cards and cash advance services (Dave, MoneyLion, etc.) When these consumers’ budgets come under stress, where will BNPL plans fit in their repayment hierarchy?

The adage during the ‘08 housing crisis was “you can sleep in your car, but you can’t drive your house to work,” a pithy if insensitive commentary on why consumers were more likely to stay current on auto loans than their mortgages (also, foreclosing on a house is a considerably more lengthy and expensive process than repo’ing a car.)

Despite the pandemic, we’ve been in an unusually benign credit environment, thanks to copious government stimulus. As the impact of those measures has faded, delinquency rates have begun to normalize.

As rates increase — with the remote possibility of inducing a recession to combat inflation — it’s likely losses for BNPL providers will increase.

What’s Wrong with Dave?

With the giddy SPAC days of 2021 behind us, it’s easy to forget the optimistic projections in all those investor presentations.

Freed from the strict requirements of IPO S-1s things got… creative!

Now, companies that SPAC’d are starting to have their first quarterly earnings as public companies, and things aren’t pretty.

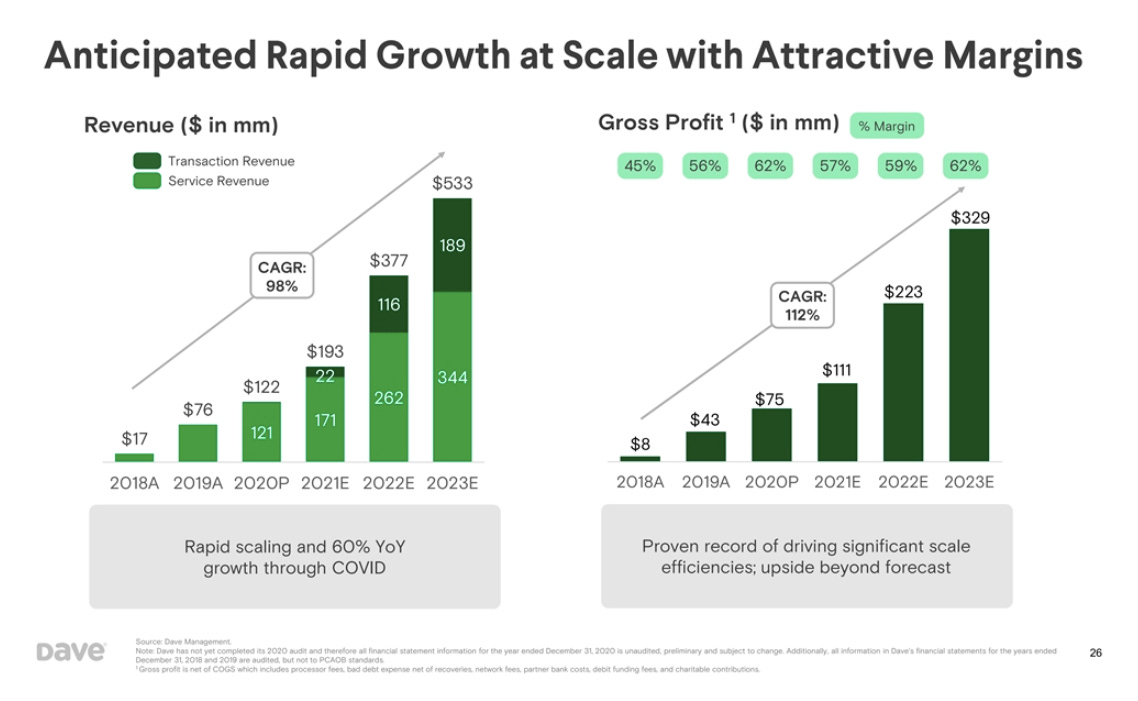

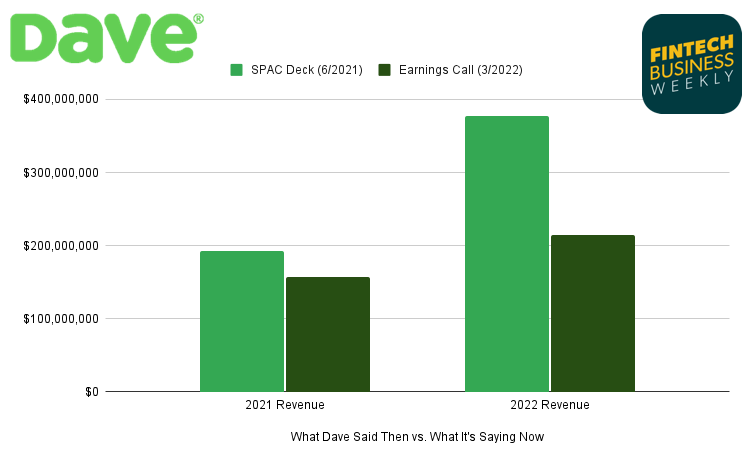

Dave, which put out its investor presentation in June 2021 (half way though the year!), forecast it would do $193 million in revenue in 2021. Instead, it booked $157 million in revenue — an ~18% miss.

Dave updated its 2022 revenue forecast from $377 million to just $200 - $230 million — a downward revision of about 43%.

Dave’s user numbers also provide reason to worry. While the company actually seems to be on track here — it boasted “over 6 million users” in last week’s quarterly earnings call — the problem is how frequently those “users” actually use Dave’s products.

{kind=link}

Though it may now have some 6 million users, only 1.51 million (~25%) use the service in a given month.

Those that are using Dave average just 4.5 transaction per month — compared to an average 25.5 transactions per month on a typical debit card and a reported 40 transactions per month for the average Chime customer.

This isn’t necessarily surprising, given Dave heavily courts users with its “no interest, no credit check” cash advance. Dave is more likely to attract users looking to use it as a payday-like loan rather than as a primary bank account.

While Dave’s quarterly earnings announcement didn’t break out revenue by source, the lower ratio of active users and the low number of transactions per user suggests Dave is more dependent on its ExtaCash (cash advance) product for revenue vs. interchange.

Dave earns revenue from ExtraCash in the form of optional user “tips” and expedited funding fees — practices that are likely to attract attention from a recently re-empowered CFPB.

Six Theories on Why Apple Acquired Credit Kudos

Any news about Apple inevitably inspires an infinite number of hot takes, and I’m no exception this week.

The news that Apple acquired UK open banking startup Credit Kudos lead to a flurry of speculation about Apple’s plans for the startup.

To better inform that speculation, it’s critical to understand what Credit Kudos actually does. While most press coverage refers to it as an “open banking” startup, the company does not provide connectivity to access bank account information (like Plaid or MX), nor does it have the capability to initiate a payment from a user’s bank account.

Instead, Credit Kudos uses third-party APIs to pull bank account data and then analyzes it to generate affordability- and credit risk-related insights — akin to Prism Data in the US, the cashflow-based underwriting-as-a-service offering from Petal.

Paired with other fintech- and identity-capabilities Apple is developing, particularly its mobile driver’s licenses in the US, could enable a number of new products and features for Apple.

With that context, here are six possibilities for how Apple could leverage the Credit Kudos acquisition in other parts of its business:

For Apple Card (US)

There was significant speculation that Apple could use Credit Kudos’ underwriting capabilities to bolster its Apple Card offering, currently only available in the US.

This is rather unlikely. In the US, Apple Card is issued by bank partner Goldman Sachs. Goldman Sachs is responsible for underwriting applicants — not Apple. Any decisions about incorporating bank account data would likely come from Goldman, and any technology partners would most likely integrate with Goldman’s tech stack directly, rather than via Apple.

Account-to-Account Payments

Also unlikely. When I first read the announcement, I misunderstood Credit Kudos’ offering as the APIs offering access to consumers’ bank account data and ability to initiate payments — as explained above, that is not the case.

While adding account-to-account payments to Apple Pay would be a logical extension of its service, that’s more likely to take place in conjunction with the launch of an Apple BNPL offering (more on that below). Apple’s acquisition of Credit Kudos doesn’t immediately give it the ability to do account-to-account payments.

For Apple Card (UK)

Apple doesn’t yet offer an Apple-branded credit card in the UK, but it’s the obvious first choice for expanding Apple Card’s footprint. Although there are plenty of differences between the US and UK in offering consumer credit, the UK is the largest most similar market (sorry, Canada), and is arguably simpler, from a regulatory perspective, than the US.

Still, if Apple expands Apple Card to the UK, it is most likely to do so via a bank partner. As such, the same logic as the US would apply: Apple’s UK bank partner would be the one underwriting the card, and thus would be the party ingesting users’ bank account data, in combination with traditional credit data, to make an underwriting decision.

An Apple Wallet PFM Tool

This also strikes me as rather unlikely but possible. Could Apple be looking to expand the functionality of Apple Wallet to some sort of Mint-esque PFM tool?

Acquiring Credit Kudos would substantially advance such an initiative — and acquiring its talent would help as well. One can imagine Wallet morphing from its current lackluster feature set to a user’s go-to destination for managing their finances. Being able to connect external accounts and gain meaningful insights about spending and cashflow would substantially bolster the usefulness of Apple Wallet.

Still, Apple tends to launch major new features in the US. A PFM offering would make more sense in connection with Apple Card, which is integrated into the Wallet app — but perhaps working with Goldman is proving more cumbersome that Apple wants, and the UK provides an alternative market to roll out and test new features?

Apple Device Subscription

Apple has long been rumored to be working on transitioning to a subscription model for iPhone hardware. The move could make the price tag of iPhones — now exceeding $1,000 for top-of-the-line models — more palatable for consumers by breaking it into a small monthly fee. A subscription model would also make Apple’s revenue more consistent — and further lock users in to the Apple ecosystem.

Apple already offers various ways to reduce or spread the cost of new phones, including trading in old equipment, carrier-related deals, financing from Citizens Bank, and financing tied to Apple Card.

Moving from external financing partners to a subscription model would give Apple more control over the terms and expand the universe of customers who are eligible.

Cashflow-based underwriting, like that which Credit Kudos offers, could be a key ingredient to offering an Apple device subscription to users, particularly those with limited credit history.

Apple BNPL

A BNPL offering from Apple has reportedly been in the works for a while now. Reportedly dubbed “Apple Pay Later,” the offering would include both shorter-term, no-cost “pay in 4” plans as well as longer-term, interest-bearing loans that would be offered through Apple’s partnership with Goldman Sachs.

If Apple intends to offer the “split pay” portion of the offering itself (and collect the merchant discount rate), cashflow-based underwriting tech like Credit Kudos would help it assess customers’ creditworthiness.

Still, the attractiveness of entering the BNPL directly has arguably declined since this news originally broke. MDRs have declined and regulatory scrutiny has increased. Perhaps Apple’s priorities on BNPL have shifted?

Something Else Altogether

None of these possibilities is a slam dunk — Apple could be up to something else altogether. And it may be awhile before whatever Apple has planned comes to market. As industry expert Simon Taylor pointed out, it was some two years between when Apple acquired Mobeewave and when that technology manifested as the ability for iPhones to accept card payments without additional hardware.

The Fintech Guide to World-Class Recovery

Sponsored content: The goal of a collections and recovery operation is to maximize profitability by efficiently recovering money lent to consumers while maintaining consumer loyalty — a tall order for fintech businesses trying to do it all in-house. But there is a win-win strategy out there, and you’ll find it in TrueAccord’s latest ebook, the Fintech Guide to World-Class Recovery.

The recovery and collection process is an opportunity for fintechs to extend the forward-thinking, consumer-centric approach that has made them successful in disrupting the status quo. This ebook provides the tools and frameworks to ensure that you’re architecting the right recovery strategy for your company for the long run.

Other Good Reads

Workers Are Trading Staggering Amounts of Data for 'Payday Loans' (Wired)

Hands-on-the-Wheel Money (Fintech Takes)

The Growing Domination Of Chime, Cash App, And PayPal In Banking (Ron Shevlin/Forbes)

Contact Fintech Business Weekly

Looking to work with me in any of the following areas?

Sponsoring this newsletter

Content collaboration or guest posting

Early stage startup looking to raise equity or debt capital

Feel free to reach out to me: jason@fintechbusinessweekly.com

Looking for ‘Drive Now, Pay Later’: Is BNPL on a Slippery Slope?

There’s more Fintech Business Weekly below for paying subscribers👇 — if you already subscribe, thank you for helping make this newsletter possible