Should Goldman Buy Affirm?

Advocates Press FDIC on "Rent-a-Bank," BlockFi's $100m Settlement, FDIC's 2022 Priorities, CFPB Highlights Changing Overdraft Practices

Hey all, Jason here.

Some people watch the Super Bowl for the competition. Some watch for the half-time show. And some watch for the ads. Those paying attention to the adverts, which reportedly run $6.5 million per 30 seconds, are bound to notice something this year: the number of crypto companies advertising.

If you’re watching, keep your eye out for ads from recently hacked Crypto.com, Coinbase, and FTX. The game is airing a bit late for me to watch live, so I’ll have to catch up tomorrow morning.

Existing subscriber? Please consider supporting this newsletter by upgrading to a paid subscription. New here? Subscribe to get Fintech Business Weekly each Sunday:

New York City’s Largest Fintech Event Returns This Spring

Sponsored content: On May 25th - 26th, LendIt Fintech USA returns to the Javits Center for 2 days of world-class content and long awaited face-to-face networking. Explore the complexities of today’s financial services industry through insightful sessions focused on the most important trends in banking and lending. Key topics include digital banking, Web3, green fintech, consumer lending, embedded finance and much more.

Save 15% on your pass with the code MEDIA15_FBW — see you there!

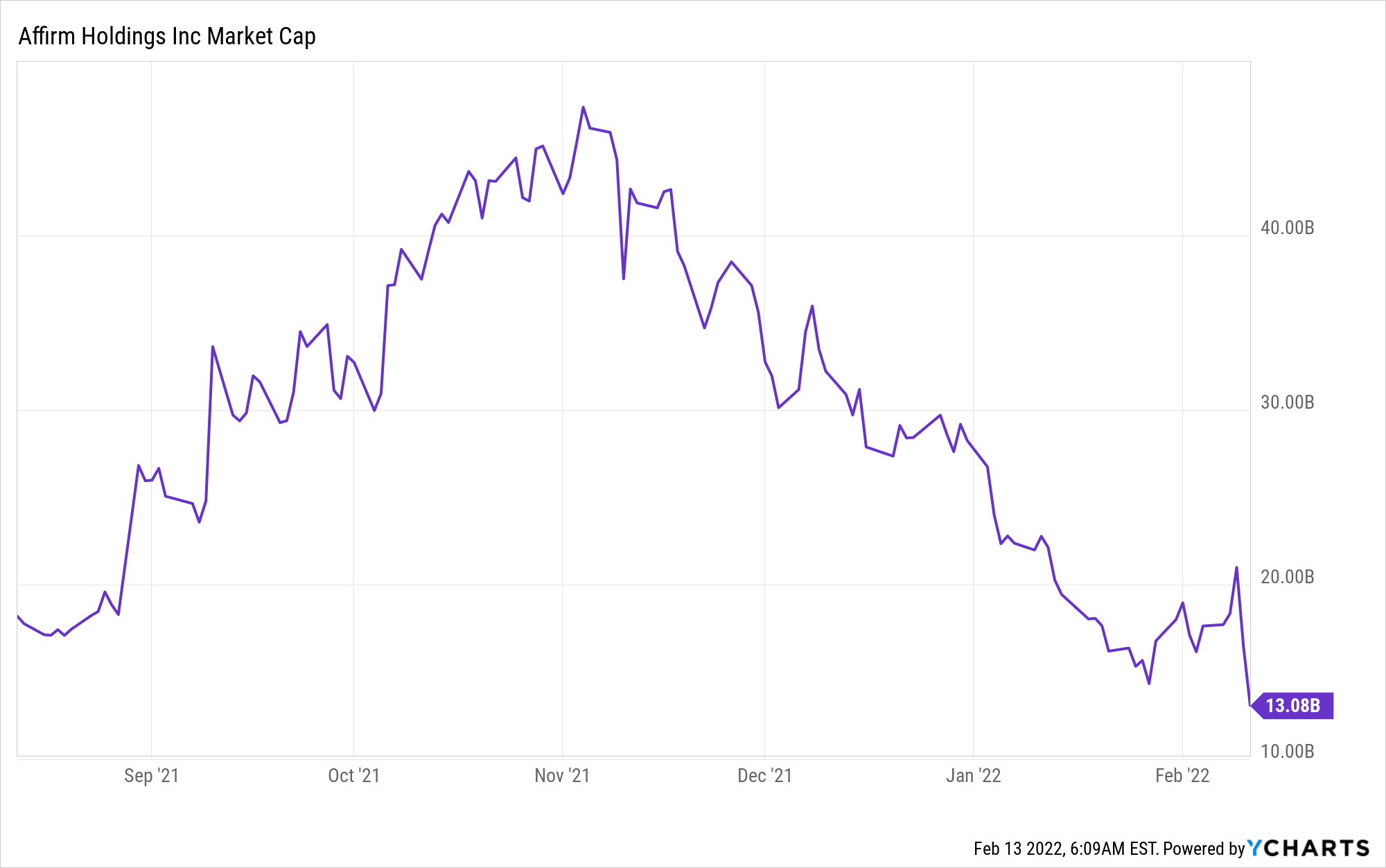

Affirm’s Stock Tanked on Increasing Costs. Should Goldman Buy It?

Who among us hasn’t sent a tweet they regretted? Though usually a poorly thought out missive doesn’t vaporize ~$8 billion in market cap (unless you’re Elon Musk).

But, to be fair to whatever social media manager pre-maturely sent Affirm’s tweet that included some of its yet-to-be-released financial results, it was the contents of Affirm’s quarterly earnings that sent the BNPL company’s share swooning, not the errant timing of a tweet.

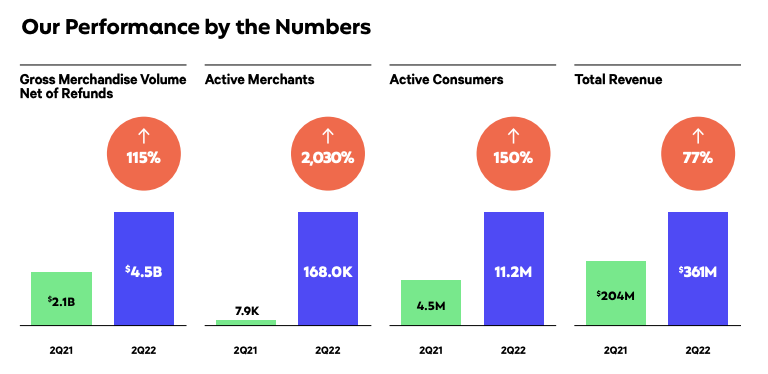

The results that sent Affirm’s shares sharply down? Despite a 77% jump in top line revenue to $361m, its losses grew to $160m — a loss of $0.57 per share vs. analysts’ estimate of a $0.32 loss per share.

Growing losses were driven by a large jump in operating costs, which more than doubled to $557m in the quarter, as sales, marketing, and administrative expenses increased.

Affirm was trading down as much as 40% by the close of market Friday, bringing its market cap to just over $13 billion.

In a market that seems primed for fintech M&A, Affirm’s newly reduced price poses an interesting question: could Affirm be an acquisition target? And, if it is, who might make sense as a buyer?

Why A Goldman/Affirm Combo Makes Sense

Affirm would make an interesting tuck-in acquisition for Goldman’s Marcus consumer business.

While, historically, Goldman has shied away from larger acquisitions, that has changed in recent years, particularly in regards to the consumer business.

It acquired Marcus’ online deposit platform from GE Capital Bank; wealth management franchise United Capital; PFM app Clarity Money, which became Marcus Insights; and, most recently, home improvement POS lender GreenSky.

The logic of the GreenSky acquisition, for which Goldman paid $2.24 billion in an all-stock deal, was pretty straightforward.

Goldman paid to acquire the customer acquisition channel GreenSky had painstakingly built: the thousands of contractors, plumbers, electricians, home improvement retailers, and doctor and dentist offices GreenSky used to offer its loans.

GreenSky would complement Goldman’s existing distribution channels. The economics of GreenSky’s business should improve as part of Goldman, with Goldman’s bank charter, low cost of funds, and ability to balance sheet the loans it originates.

A similar case could be made for a hypothetical Affirm acquisition.

Goldman’s attempt to launch its own BNPL offering, MarcusPay, never expanded beyond initial launch partner JetBlue. Goldman is working on a BNPL with credit card partner Apple, but that also has yet to launch.

Acquiring Affirm could bring its 11.2 million active users onto the Marcus platform. More importantly, in one fell swoop, Goldman would onboard 168,000 merchants — including Amazon and Shopify’s network of merchants — as distribution channels for POS loans:

Goldman would also acquire pay-in-four capabilities it currently lacks, which could provide potential synergies with its forthcoming Apple BNPL or Marcus checking offerings.

Functionality of Affirm’s yet-to-launch Affirm Debit+, a “decoupled” debit card that enables users to split pay nearly any transaction, could be folded into Goldman’s planned Marcus checking product.

And, like in the GreenSky deal, the unit economics of Affirm’s business would likely improve as part of a bank vs. the bank partnership model it currently uses to write loans.

Goldman has repeatedly talked about Marcus as a “platform.” Supplementing its current capabilities with Affirm’s network of merchants, particularly Amazon and Shopify, dovetail neatly with Goldman’s efforts to date.

BlockFi to Pay $100 Million to Settle with SEC & States, Will Cease Offering “Interest” Accounts

BlockFi, which has been under scrutiny from numerous state securities regulators, will pay a $100 million settlement and stop offering its “interest” accounts to new customers, Bloomberg is reporting.

BlockFi is far from the only player to attract regulators’ scrutiny for offering high-yields on users’ crypto deposits. Coinbase planned to offer a similar product, dubbed Coinbase Lend, but canceled plans to do so after warnings from the SEC. Other crypto firms, like Celsius and Gemini, offer similar products, and are reportedly under SEC scrutiny.

Companies like BlockFi and Coinbase are easy enough for regulators to pursue actions against: they’re centralized and US based. What’s less clear is how regulators plan to address offshore entities, which may fall outside of their jurisdiction, or DeFi protocols, which have no centralized entity to pursue an enforcement action against.

Consumer Advocates Press FDIC to End “Rent-a-Bank” Fintech Partnerships

With the change in control at the FDIC, consumer advocacy groups wasted no time in pressing the new acting chair to end so-called “rent-a-bank” schemes.

The battles around fintech-bank partnerships, particularly those used to originate loans at rates over 36%, are ongoing — and not particularly clear cut.

While Democrats aligned to repeal the Trump-era “true lender” rule, the action had minimal impact, as the rule only covered national, OCC-regulated banks. The rule change had no impact on state licensed banks favored by fintech lenders.

Last week, the US District Court of Northern California upheld the OCC and FDIC’s “valid when made” rules, dismissing state AGs’ challenge — but the preservation of that rule may actually lead to greater scrutiny of fintech-bank partnerships.

Acting Comptroller Michael Hsu made a brief statement on the decision, highlighting that the improved legal clarity should not be used to facilitate “rent-a-bank” arrangements (emphasis added):

“Today, the district court affirmed the validity of the OCC’s rule, which provides that when a national bank or state or federal savings association sells, assigns, or otherwise transfers a loan, the interest permissible before the transfer continues to be permissible after the transfer.

This legal certainty should be used to the benefit of consumers and not be abused. I want to reiterate that predatory lending has no place in the federal banking system. The OCC is committed to strong supervision that expands financial inclusion and ensures banks are not used as a vehicle for ‘rent-a-charter’ arrangements.”

“Valid when made” applies only in cases where a bank originates a loan at a legally permissible interest rate in its home state and then sells the loan; if a regulator or consumer successfully argues a non-bank fintech, not a partner bank, originated a given loan, the rule wouldn’t apply.

That line of argument is exactly the one Washington DC’s attorney general pursued against OppFi and, more recently, Elevate.

Last week, Elevate reached a $3.75 million settlement with Washington DC for offering loans in excess of DC’s 24% usury cap. Elevate had operated in DC in conjunction with its bank partners, Utah-chartered FinWise and Kentucky-chartered Republic Bank and Trust. DC argued that Elevate, not its bank partners, was the “true lender,” and thus the loans did not enjoy preemption and were in violation of DC’s rate cap.

While local AGs fight jurisdiction by jurisdiction, consumer advocacy groups like the Center for Responsible Lending (CRL), Woodstock Institute, and NAACP are exerting pressure at the national level by encouraging the FDIC, which oversees state-licensed banks, to shut down the practice.

The group’s letter argued that state rate caps are the best way to protect consumers (emphasis added):

“Federal supervision and enforcement of the laws that apply to banks are no substitute for the state rate caps that rent-a-bank schemes evade. State interest rate limits are the most effective way to protect consumers from unfair, abusive and unaffordable loans in the absence of a national interest rate limit.”

and further argued that partnering with fintechs originating loans in excess of state usury caps poses “legal, safety and soundness, and reputational risks” to banks.

The group’s letter argued “rent-a-bank” schemes (emphasis added):

“Are an abuse of the bank charter to facilitate loans for non-banks that are the true lender, helping them evade state laws.

Lead to abusive lending practices as they divorce lender and borrower incentives, allowing lenders to succeed while causing severe harm to consumers.

Pose a range of legal, safety and soundness, and reputational risks to banks.

Carry a high risk of jeopardizing compliance with several federal laws, including the Military Lending Act, Community Reinvestment Act, the Equal Credit Opportunity Act, the Electronic Fund Transfer Act, the Fair Debt Collection Practices Act and the Fair Credit Reporting Act.

Contradict principles of responsible lending that banking agency guidance has consistently promoted.”

The Fintech Guide to World-Class Recovery

Sponsored content: The goal of a collections and recovery operation is to maximize profitability by efficiently recovering money lent to consumers while maintaining consumer loyalty — a tall order for fintech businesses trying to do it all in-house. But there is a win-win strategy out there, and you’ll find it in TrueAccord’s latest ebook, the Fintech Guide to World-Class Recovery.

The recovery and collection process is an opportunity for fintechs to extend the forward-thinking, consumer-centric approach that has made them successful in disrupting the status quo. This ebook provides the tools and frameworks to ensure that you’re architecting the right recovery strategy for your company for the long run.

Other Good Reads

Don’t Build Branches in the Metaverse (Fintech Takes)

The Rabbit Hole Beneath the Crypto Couple is Endless (Vice)

Marketplace suspends most NFT sales, citing 'rampant' fakes and plagiarism (Reuters)

The 17 Fintechs Most Likely to Get Acquired in 2022 (Business Insider)

Contact Fintech Business Weekly

Looking to work with me in any of the following areas?

Sponsoring this newsletter

Content collaboration or guest posting

News tip or story suggestion

Early stage startup looking to raise equity or debt capital

Feel free to reach out to me: jason@fintechbusinessweekly.com

Looking for CFPB Highlights Changing Overdraft & NSF Policies and FDIC’s 2022 Priorities?

There’s more Fintech Business Weekly below for paying subscribers👇 — if you already subscribe, thank you for helping make this newsletter possible