Klarna's 2021 Earnings; Learn Now Pay Later

Walmart's US/Mexico Remittances, CFPB's Medical Debt Report, Burgers & Bitcoin, New Mexico's 36% APR Cap

Hey all, it’s Jason.

I’m wrapping up this week’s newsletter from Mexico City (yes, again), where I’ll be spending a couple days before heading down to Oaxaca for the rest of the week. I drafted most of this on the plane, so please forgive any typos or longer and more convoluted than normal sentences!

Existing subscriber? Please consider supporting this newsletter by upgrading to a paid subscription. New here? Subscribe to get Fintech Business Weekly each Sunday:

NYC Fintech Week: April 18th - 22nd

Exciting news! I’ll be in New York for New York Fintech Week this April. I’ll also be presenting a Fintech Master Class with none other than Alex Johnson of Fintech Takes, in which we will take a critical look at the Future of Consumer Lending.

Alex and I will break down five key themes that will impact consumer lending in 2022, including the changing macro environment, bank charters and M&A, as-a-service and APIs, the changing role of credit bureaus, and, of course, BNPL.

Learn Now, Pay Later: In Quest for Growth, BNPLs Finance Dubious For-Profit Education Credentials

As BNPL has exploded in the past couple of years, it has proliferated from a financing option for relatively small retail purchases to seemingly every corner of consumer commerce. Want to pay for your pizza in installments? No problem!

But in a potentially more pernicious tie-up, numerous BNPL companies have partnered with for-profit education companies that aggressively market their programs, including by making income- and employment-related claims that may not be backed up by data.

Last week, the Student Borrower Protection Center (SBPC) released a report highlighting the practice.

According to the SBPC, BNPLs constitute a form of ‘shadow’ student loan debt — all the more problematic, as it argues the programs offering the financing are often unaccredited and of dubious value to students. SBPC found:

“Companies offering ‘Buy Now, Pay Later’ point-of-sale credit have flooded the shadow student debt market, and they are now propping up a wide array of dubious for-profit schools. BNPL providers appear to have rapidly emerged as sources of quick, risky point-of-sale shadow student debt for borrowers at a startling range of questionable for-profit schools and educational institutions.

The SBPC’s investigation revealed that BNPL options from companies including Affirm, Afterpay, Klarna, Sezzle, Shop Pay, Uplift, and Zip (formerly Quadpay) are available as a form of student loan at more than 50 apparently unaccredited and/or unregulated for-profit schools, likely pointing to an even larger trend.”

The SBPC’s research found BNPL offered as a form of student loan to pay for classes in fields like cosmetology, outdoor survival, reiki, information technology, midwifery, wigmaking, real estate brokerage, eyebrow microblading, and more.

And while the SBPC previously specifically examined use of PayPal Credit for financing questionable for-profit coursework, it found that, since its initial report, the number of programs offering PayPal Credit (longer term financing) or pay-in-4 had continued to grow:

“PayPal has failed to rein in schools’ reliance on PayPal Credit as a form of shadow student debt, and is instead now growing its support of questionable for-profits through BNPL.

Despite PayPal’s promise to rein in PayPal Credit, more than one third of the dubious for-profit schools identified in the SBPC and its partners’ August 2020 letter appear to still offer this form of revolving financing as a variety of student loan, some of them even more prominently than before.

Further, new school partners appear to be actively introducing PayPal Credit as a method of point-of-sale tuition financing, and many schools have also begun to offer PayPal’s new BNPL product for the same purpose.

These findings imply that borrowers now face massive risks in point-of-sale tuition financing related to PayPal not just as it pertains to PayPal Credit, but from the combination of PayPal Credit, PayPal’s BNPL product, and a growing lack of credibility from the company.”

Klarna’s 2021 Report: GMV Hits $80 Billion, but Credit Losses Nearly Double

Klarna released its 2021 annual report, showing growing credit losses as it reaches for continued international growth. Gross merchandise volume (GMV) jumped 42% to $80 billion. Net operating income increased 38% from 2020 to 13.75 billion Swedish krona ($1.46 billion), according to Bloomberg (confusingly, Reuters reported a 6.85 billion krona operating loss in 2021, which I couldn’t tie back to figures in the actual report.)

The US is a key focus area for Klarna. It saw a whopping 71% growth in US consumers, bringing the number to 25 million. Klarna now partners with 30 of the top 100 US retail brands.

As Klarna has grown, so too has its credit losses, which nearly doubled from 2.5 billion kronor in 2020 to 4.6 billion kronor ($487 million) in 2021. Klarna described the increase as “a direct result of our expansion and the increased volume of new consumers, rather than a deterioration of the portfolio.”

BNPL Sector Continues to Consolidate, Diversify in Quest for Growth While Preserving Margins

After experiencing explosive growth in the last couple of years, the BNPL space appears to be entering a consolidation phase — Block acquired AfterPay, Zip acquired Quadpay and Sezzle, Alliance Data acquired Bread, and I imagine more deals are forthcoming.

Increased competition, particularly PayPal’s entrance to the space, has begun to compress merchant discount rates, which previously could reach as high as 6-8%.

PayPal charges the same rate for a merchant to offer a pay-in-4 plan as to process a typical card transaction — just 3.49% + $0.49. As BNPL features become commoditized, companies that began as ‘BNPL-first’ offerings are searching for ways to build differentiated, defensible offerings while growing their geographic footprint.

Both PayPal and Affirm are re-positioning themselves as “superapps,” offering additional financial products like savings accounts, stocks, and crypto.

But 17-year old Klarna has arguably gone further, faster. The company has its Swedish banking license, giving it access to cheaper sources of funding than competitors — particularly important given coming interest rate hikes.

Klarna has also mades strides in moving from just a payment option at checkout to a consumer destination in and of itself. Like other BNPLs, Klarna has sought to move ‘up funnel’ by positioning its website and app as a shopping destination. According to its 2021 annual report, the Klarna app is its single biggest source of GMV across the Klarna ecosystem.

Klarna has also made significant progress positioning itself not just as a ‘buy now, pay later’ company, but as a payment network. Klarna says 40% of its transaction volume uses its “Pay Now” option, and it expects that rate to reach 90% for in-store transactions. Behind the scenes, payments can be processed via “account-to-account” payments, in many cases avoiding card payment networks altogether. This is possible because of Klarna’s acquisition of European payment network Sofort and partnership with GoCardless to power account-to-account payments in the US.

As BNPLs compete to win customer share of wallet, they’ve necessarily diversified away from the original pay-in-4 formulation. But with the introduction of a physical payment card with pay-in-30 terms and a rewards scheme, in many ways, Klarna begins to resemble the credit card industry BNPL ostensibly sought to disrupt.

CFPB: 20% of American Households Struggle with Medical Debt

At this point in fintech, it’s almost a cliché to talk about “financial health.” While this positioning is an improvement from earlier iterations, namely “financial literacy,” which carries a certain blame-the-victim connotation, when fintechs talk about financial health, it tends to be siloed to the context of the specific product(s) the company offers: checking accounts, credit, investing, and so on.

Not that we should need reminding, but, for the typical American household, a major driver of financial insecurity continues to be the cost of medical care. And while insurance coverage has improved since the passage of the Affordable Care Act, in 2020, 8.6% of Americans, or about 28 million people, remained uninsured.

Americans who are un- or underinsured are more likely to delay seeking care and, when they do, pay more for it. Provider pricing practices give discounts to insured patients seeking care with contracted providers, creating the perverse situation where those least able to afford it often end up paying more for the same services.

Even with insurance, the cost of care can be substantial. And because of labyrinthine billing and insurance payment processes, many Americans can end up with medical bills in collections due to delayed or denied payments from insurance companies.

The result is a whopping 20% of Americans who report carrying some form of medical debt.

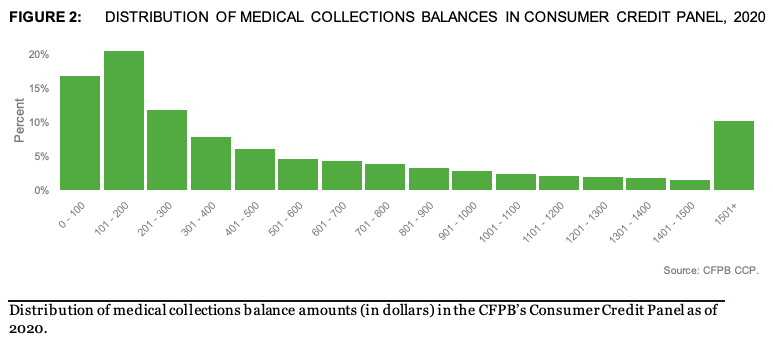

The CFPB’s report, based on analysis of medical debt in collections that is reported to major credit bureaus, found that medical collections tradelines appear on 43 million credit reports. It also found that 58% of bills in collections that show up in credit reports are medical bills.

Looking at medical debt that ends up on the bureaus is almost surely an undercount. It doesn’t include debt that consumers owe to providers that hasn’t been placed for collection or reported to bureaus. Nor does it include consumer debt incurred via financing mechanisms, like credit cards or point-of-sale loans, that could end up in collections, but wouldn’t appear as a medical debt tradeline.

The CFPB’s analysis found the amount per tradeline was generally low. This analysis, however, likely understates a typical consumers’ overall burden, as consumers with medical debt often have more than one tradeline in collections, and, as mentioned above, may have others debts that don’t appear in bureau data.

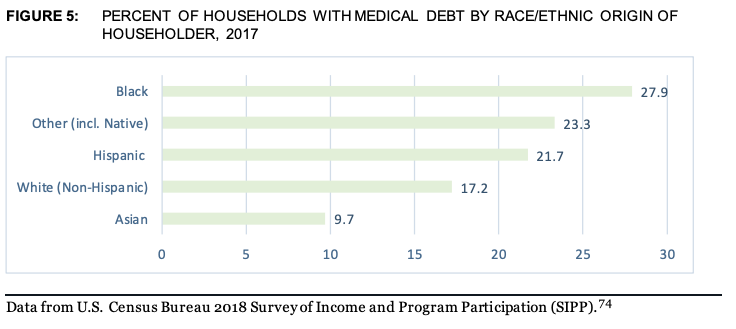

Perhaps unsurprisingly, the impact of medical debt has disproportionate impacts by race/ethnic origin. Black and Hispanic households are significantly more likely to owe medical debt than similarly positioned white households.

These debts take a toll. Besides well-documented impacts on consumers’ ability and willingness to access needed healthcare, medical debt tradelines can negatively impact consumers’ credit scores, and thus their ability to access credit, qualify for an apartment, or even get a job.

The CFPB argues that medical debt collections are a less reliable predictor of future payment behavior and thus can penalize otherwise responsible consumers. While newer versions of popular scoring models like FICO and Vantage take this into account by discounting or ignoring medical collections tradelines, not all potential creditors use the latest models.

Even if creditors are using updated models that handle medical debt differently, most operate proprietary scoring models in addition to off-the-shelf models from FICO and Vantage. There is little to no population level visibility and analysis into how lenders’ custom models impact applicants with medical debt and collections.

The CFPB’s report ends with a set of recommendations, including determining whether unpaid medical bill data should be used in credit reports in any manner.

According to its release, the CFPB intends to:

“Hold credit reporting companies accountable: Federal law requires credit reporting companies to have reasonable procedures in place to assure that medical debt on consumer reports is accurate. Those procedures must include, if necessary, taking action against furnishers who routinely report inaccurate information. If furnishers, of medical debt or otherwise, are contaminating the credit reporting system with inaccurate reports, the CFPB expects the Big Three agencies to cut off their access to the system.

Work with federal partners to reduce coercive credit reporting: The CFPB is working with the U.S. Department of Health and Human Services to ensure that patients are not coerced into paying bills more than the amounts due.

Determine whether unpaid medical billing data should be included in credit reports: The CFPB will conduct additional research on how medical billing, collections, and credit reporting practices affect patients and families. Informed by those findings, the CFPB will assess whether consumer credit reports should include data on unpaid medical bills.”

Walmart Latest to Add US/Mexico Remittances

Walmart is the latest company to make a bet that offering cheaper remittances from the US to Mexico will pay dividends on both sides of the border. The company has revived its Walmart2Walmart offering, after pausing it in 2018.

Recent months have seen a number of fintechs focus on remittances as a wedge feature to gain market share.

Revolut has made US/Mexico remittances a cornerstone of its strategy in both countries. Coinbase recently added crypto- and stablecoin-powered remittances, with the option to collect cash at 37,000 retail locations in Mexico. Even Meta (Facebook)’s efforts for its fledgling wallet attempt to leverage the strategy, as it pilots its Novi wallet in the US and Guatemala.

Walmart has the notable advantage of its existing retail infrastructure on both sides of the border. This should enable it to conduct physical cash in on the US side and cash out on the Mexican side at lower cost than if it had to rely on third-party retailers.

Physical cash remains the dominant form of payment in Mexico, but adds substantial expense to the remittance process.

Walmart claims its transactions, powered by establishment player Ria, could cost as little as $2.50 and be as much as 50% cheaper than existing options:

“Walmart (NYSE: WMT) is making it significantly cheaper for its customers to send money to Mexico. Customers can now send money from any Walmart store in the U.S. to any Walmart store in Mexico for as little as $2.50 per transaction through its Walmart2Walmart money transfer program — at least 50% lower than similar offerings on the market.

This game-changing low fee marks another major milestone for the retailer as it remains committed to providing more inclusive and affordable financial solutions for all customers, including unbanked or underbanked households that rely on services like wire transfers for everyday money management.”

FT Partners: February Report

FT Partners released its February fintech report, which is always worth a read. I always spot something in it that I had missed — in this month’s report, for instance, that kin, in the hard-hit insurtech space, canceled its pending SPAC deal.

The report also includes a thorough analysis of public market fintech valuations, which is well worth a review, given the recent turbulence in the sector (see pages 23 - 43).

Despite the public market upheaval, private fundraising activity remains robust, with 301 deals tracked in February (though many of these may have been negotiated before market volatility really picked up in January):

Other Good Reads

Breaking Down Banking-as-a-Service (Fintech Takes)

Long Take: On Ukraine and the economic sanctions of Russia (Fintech Blueprint)

Financial Warfare (Net Interest)

Contact Fintech Business Weekly

Looking to work with me in any of the following areas?

Sponsoring this newsletter

Content collaboration or guest posting

News tip or story suggestion

Early stage startup looking to raise equity or debt capital

Feel free to reach out to me: jason@fintechbusinessweekly.com

Looking for stories on Burgers & Bitcoin or New Mexico's 36% APR Cap?

There’s more Fintech Business Weekly below for paying subscribers👇 — if you already subscribe, thank you for helping make this newsletter possible