Dave & MoneyLion: 10-K Showdown

California EWA Report & New Regs To Define Tips, Subscriptions As "Charges"; Apple Pay Later Rolling Out; EWS Preps Paze Wallet Pilot

Hey all, Jason here.

Tired of reading about SVB and responses from legislators/regulators? You’re in luck, this week’s newsletter is certified 100% SVB-free! If that’s what you’re looking for, find FDIC Chair Martin Gruenberg’s prepared testimony to the Senate Banking Committee here and Fed Vice Chair for Supervision Michael Barr’s prepared testimony here.

Existing subscriber? Please consider supporting this newsletter by upgrading to a paid subscription. New here? Subscribe to get Fintech Business Weekly each Sunday:

Join us for the future of fintech at Fintech Nexus USA!

Sponsored content: Connect with top industry leaders, innovators, and investors as they discuss topics, such as digital banking, fraud, credit, lending, payments, blockchain, AI, regulation, and more. This is the place to network with senior professionals and explore new business opportunities. Register now for a chance to be part of the premier fintech event of the year!

Dave vs. MoneyLion: 10-K Showdown

Dave and MoneyLion, two US neobanks that went public via SPACs, announced their full year 2022 results earlier this month.

And while both companies managed to contort their metrics to paint a positive-sounding picture — both refer to “record” performance in their earnings releases — drilling in to the earnings reports reveals a far more questionable state of affairs.

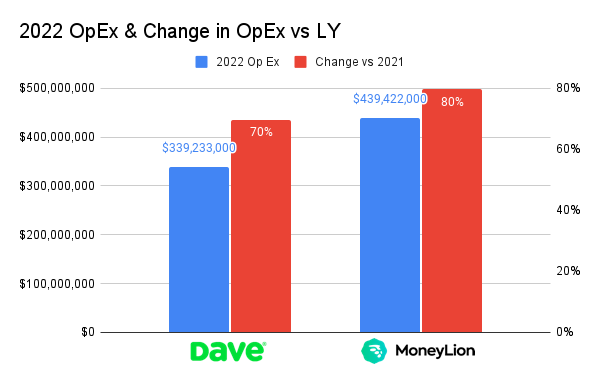

Both Dave and MoneyLion posted sizable increases in top line revenue — 34% and 99% growth over 2021, respectively.

But, that growth in revenue came along with sizable jumps in operating expenses, driven by increases in provision for loan losses, employee compensation and benefits, and marketing expenses at both companies.

MoneyLion saw operating expenses jump by 80% — a somewhat slower pace of growth than revenue — whereas Dave saw its expenses jump 70%, more than swamping its increase in top line revenue.

Unsurprisingly, the result is soaring losses at both companies.

Looking at net losses before other income/expenses, which excludes interest income/expense, change in value of warrants/convertible notes, goodwill impairment adjustments, and other income, MoneyLion posted a loss of just shy of $100 million and Dave lost a whopping $134 million.

While Dave looks slightly better on a GAAP basis, MoneyLion looks substantially worse, owing primarily to a $137 million goodwill impairment charge and about $30 million in interest expense.

The goodwill impairment loss seems to be linked to MoneyLion’s 2021 acquisition of affiliate marketplace Even Financial. At the time it was announced, the companies claimed the deal valued Even at $440 million — based on a MoneyLion share price of $10.

MoneyLion’s current share price of $0.57 would imply Even is worth about $35 million, rather than $440 million, based on the terms of the acquisition.

Not only were both Dave and MoneyLion loss making for 2022, both their losses are growing. Dave’s net loss (before other expense/income) ballooned by 187% year over year, growing to some $134 million; MoneyLion’s grew by a more modest 35% to a $98 million loss in 2022.

Looking at user-level metrics is slightly more encouraging. Dave boosted its count of users by 38% over 2021 to 8.3 million. However, only 1.9 million Dave customers are actually active in a given month — a proportion which declined from the year prior (edit: the absolute number of active customers increased from 1.6 to 1.9 million; the proportion considered to be “monthly transacting members” declined from 25.1% to 22.9%)

At first glance, MoneyLion put up impressive growth numbers, nearly doubling its number of customers from 2021 to 6.5 million. A closer read of the definition of “customers” reveals that it includes “customers that are monetized through [MoneyLion’s] marketplace and affiliate products.”

In practice, this means if a user finds, say, a Petal credit card through MoneyLion’s marketplace, MoneyLion is counting that user as a “customer” — even if it has no other ongoing relationship with the user.

On a revenue and cost of customer acquisition basis, MoneyLion at least appears to have workable unit economics, showing $52 in annual revenue per user vs. $33 in CAC, whereas, in 2022, Dave spent on average $30 to acquire customers who generated, on average, $25 in revenue:

Increasingly, a consensus is forming that interchange alone is likely not a viable business model. MoneyLion arguably has done a better job than Dave and other neobanks at expanding its own product stack and monetizing through partners/affiliates.

This is all the more important, as the customer segments Dave and MoneyLion serve skew lower-income and subprime, and thus are particularly challenging to lend to, even in a relatively benign economic climate. Persistent inflation, rising interest rates, and the threat of recession only increase the challenge.

In 2022 as its lending grew, Dave set aside about $66 million in provisions for loan losses, or about twice its provision from 2021. MoneyLion’s provision grew by 64% to about $100 million.

Dave’s total amounts charged off (net of recoveries) for the year were about $54 million, while MoneyLion charged off about $84 million in unrecoverable debt.

Diving deeper into MoneyLion’s delinquency metrics paints an even worse picture of its users’ ability to keep current on their obligations. While a relatively high 90% of Instacash receivables were current at the end of 2022, over 13% of receivables from MoneyLion’s credit building loan product were 31 or more days delinquent.

Delinquency rates on subscriptions and fees users owed to MoneyLion were even higher — about 24% of fee revenue was 31 or more days past due; and about 27% of subscription dues were 31 or more days late.

The rising rate environment has hit valuations for all assets, and “growth” sectors like tech and fintech have been particularly hard hit. Since completing their SPACs and beginning to trade, MoneyLion has lost about 94% of its market value, while Dave has shed 98% of its value.

Currently, Dave is worth about $72 million, and MoneyLion is worth about $128 million:

Do Dave & MoneyLion Have A (Realistic) “Path to Profitability”?

In each of their earnings presentations, Dave and MoneyLion include their “plans” on how to reach profitability before they burn through the cash they have on hand. Both rely on presenting adjusted EBITDA, which strips out significant recurring expenses that will continue to impact their cashflow.

MoneyLion’s pitch on how it will get to profitability is… light on details (or maybe they’re just using the word ‘profitability’ differently than I’m used to?)

The $15 million in annualized savings it touts achieving in Q4 is a drop in the bucket against the $439 million in operating expenses incurred in 2022.

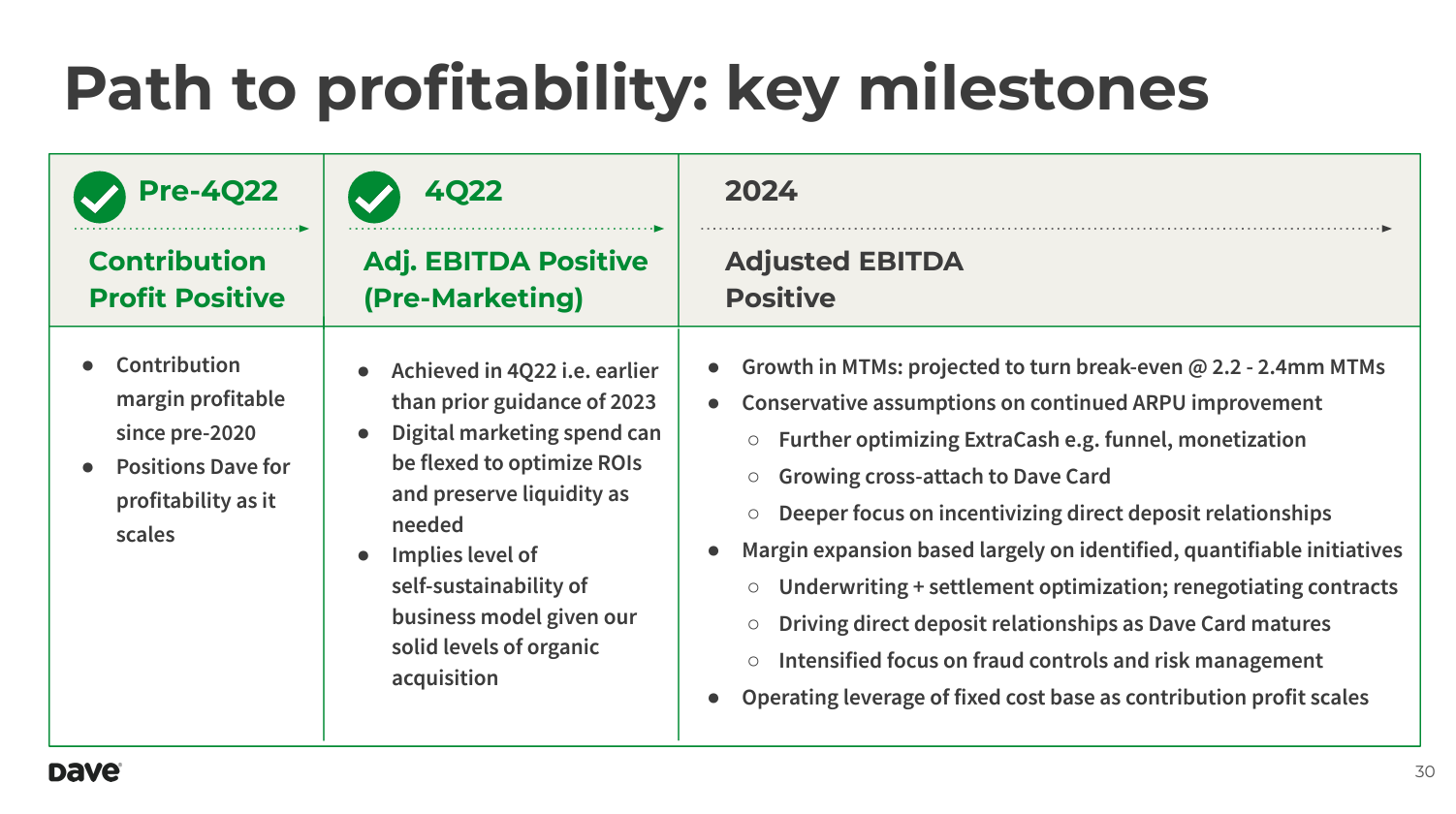

Meanwhile, Dave touts become “adjusted EBITDA positive (Pre-Marketing),” without mentioning that “marketing” is its second-largest expense, after employee compensation, coming in at $69 million in 2022.

Dave does provide greater specificity on initiatives to help the company reach profitability: growing its number of active users, driving ARPU improvements by cross-selling Dave Card (banking) and optimizing ExtraCash (improving conversion rate), increasing users’ direct deposit attachment rate, and by improving underwriting, fraud, and risk management.

What’s less clear is exactly how it will achieve these improvements, and if they will be significant enough to get Dave’s business model to economic viability.

2023 Banking-as-a-Service & Partner Bank Market Analysis

It’s been about six weeks since I released my first research report, focusing on partner banks and banking-as-a-service, and I’ve been pleasantly overwhelmed at the positive reception. The BaaS space is continuing to evolve quickly, and hopefully I’ll have the opportunity to release a 2024 update!

In the meantime, here’s what readers are saying about the report:

(this is high praise from Ron, I swear!)

A New California Regulation Will Define “Tips” And Subscription Fees As Finance Charges. What It Could Mean.

While several national banking stories have, understandably, garnered most of the headlines lately, other regulatory initiatives grind on.

California’s financial services regulator, the Department of Financial Protection and Innovation (DFPI), undertook an initiative in 2021 to gather data from a variety of earned wage access companies (EWA).

It struck agreements with both “employer-integrated” and “direct-to-consumer” EWA companies — a group that included Even (subsequently acquired by Walmart’s fintech ONE), Earnin’, Brigit, Payactiv, and Branch — to collect data from the companies.

While all of the companies offer products designed to enable users to advance/borrow small amounts of money for short periods of time, they take different approaches to charging borrowers, including “tips,” various types of fees, and/or subscriptions.

The DFPI’s report stemming from this data collection effort was released earlier this month and contains a number of interesting data points.

Per the report’s executive summary (emphasis added):

There was a total advanced amount of $765 million reported by responding companies.

For the 5.8 million transactions completed by tip-based companies, providers received tips 73% of the time.

The average annual APR was 334% for tip companies and 331% for the non-tip companies.

Tips generated a total of $17.55 million in revenue, and optional fees generated $6.24 million.

When a tip was provided by the consumer, the average tip amount was $4.09.

Most advance amounts (80%) are between $40 and $100.

The average quarterly growth rate for EWA transactions was 17%.

The average time for consumers to repay was 10 days.

Among the companies that reported the advanced amount as percent of paycheck, it ranged from 6% to 50% of pay.

The transaction point of receiving and repaying the funds represented 67% of complaints from EWA customers.

The DFPI’s analysis found the average EWA user took ~8.5 advances per quarter; assuming a bi-weekly or semi-monthly pay schedule, which are most common in the US, that would mean a “typical” user took 1-2 advances per pay cycle (caveat that the average may obscure important differences in the distribution of frequency of use.)

While the apparent frequent use may raise alarm bells about “sustained use,” it’s difficult to evaluate whether such use is welfare-enhancing or destructive for consumers.

What matters is what they would do absent the ability to use EWA — overdraft their bank account? Use a payday loan? It’s entirely possible that, absent workers earning more or lowering their monthly costs, EWA is the “least bad option” when compared to other small-dollar, short-duration products.

Perhaps the most interesting takeaway was, despite the different monetization models, the effective APR of “tip” vs. non-tip based products was roughly comparable.

Proposed Rule Would Define Advances As Loans, “Tips” and Subscription Fees as Charges

A proposed rule that is currently in its comment period, PRO 01-21, would, among other things, require certain business to register with and report data to the DFPI, including for income-based advances, education financing, debt settlement, and student debt relief providers.

In addition to the registration and reporting requirements, there are a couple of definitions and clarifications that have the potential to significantly impact companies extending income-linked financing — products that include income share agreements (ISAs) and EWA (both employer-integrated and DTC) — as well as companies that incorporate “tips” as part of their business model.

First, part 1461 of the proposed regulation explicitly defines such products as “loans” under California law, stating in part (a):

Any advance of funds to be repaid in whole or in part by the receipt of a consumer’s wages, salary, commissions, or other compensation for services, is a sale or assignment of wages and a loan subject to the California Financing Law, regardless of the funding provider’s means of collection, whether the provider has legal recourse if the provider is unable to collect the amount it advanced, or whether the consumer has the right to cancel collection of the amount advanced

And further defines consumers receiving such advances as “borrowers” under California law.

Second, part 1465 clarifies that “voluntary or optional” payments — like so-called “tips” — are to be considered a “charge” for the purposes of California law, stating:

A voluntary or optional payment, including, without limitation, a tip or gratuity, paid by a borrower to a licensee or any other person in connection with the investigating, arranging, negotiating, procuring, guaranteeing, making, servicing, collecting, and enforcing of a loan, is a charge under Financial Code section 22200.

Under the proposed rule, “charges” also include, without limitation, subscription fees, expedited funding fees, and account transfer fees.

While California’s treatment of “tips” and subscription fees has no direct bearing on how federal regulators treat them — think TILA Reg Z — treating “tips” and subscriptions as charges under California law could have knock-on impacts as far as whether or not certain tip- and subscription-based products comply with California usury limits.

Other Good Reads

Your Spending Habits Are All In Your Head (UChicago Booth)

Apple Launches Apple Pay Later And It’s Going To Be A Winner (Ron Shevlin/Forbes)

Lending and the Engineering of Chaos (Chaos Engineering)

About Fintech Business Weekly

Looking to work with me in any of the following areas? Email me.

Fintech advising & consulting

Sponsoring this newsletter

News tip or story suggestion — reach me on Signal at +1-316-512-1571

Early stage startup looking to raise equity or debt capital