Affirm's Earnings: Funding Costs Soar 223% Year Over Year

Daylight Shuts Down, Colorado Bill Could Block High APR Fintech Lenders, Five Takeaways From Fed's Economic Well Being Report

Hey all, Jason here.

Happy Memorial Day to all my US-based readers! I hope you’re enjoying a long weekend. Spring is in full swing in the Netherlands, and I’m immensely happy to be back.

If you missed the email last week, you still have three days to snag my 2023 Banking-as-a-Service Market Analysis for 20% off — get it before the price goes up on Wednesday!

Existing subscriber? Please consider supporting this newsletter by upgrading to a paid subscription. New here? Subscribe to get Fintech Business Weekly each Sunday:

Affirm's Earnings: Funding Costs Soar 223% Year Over Year

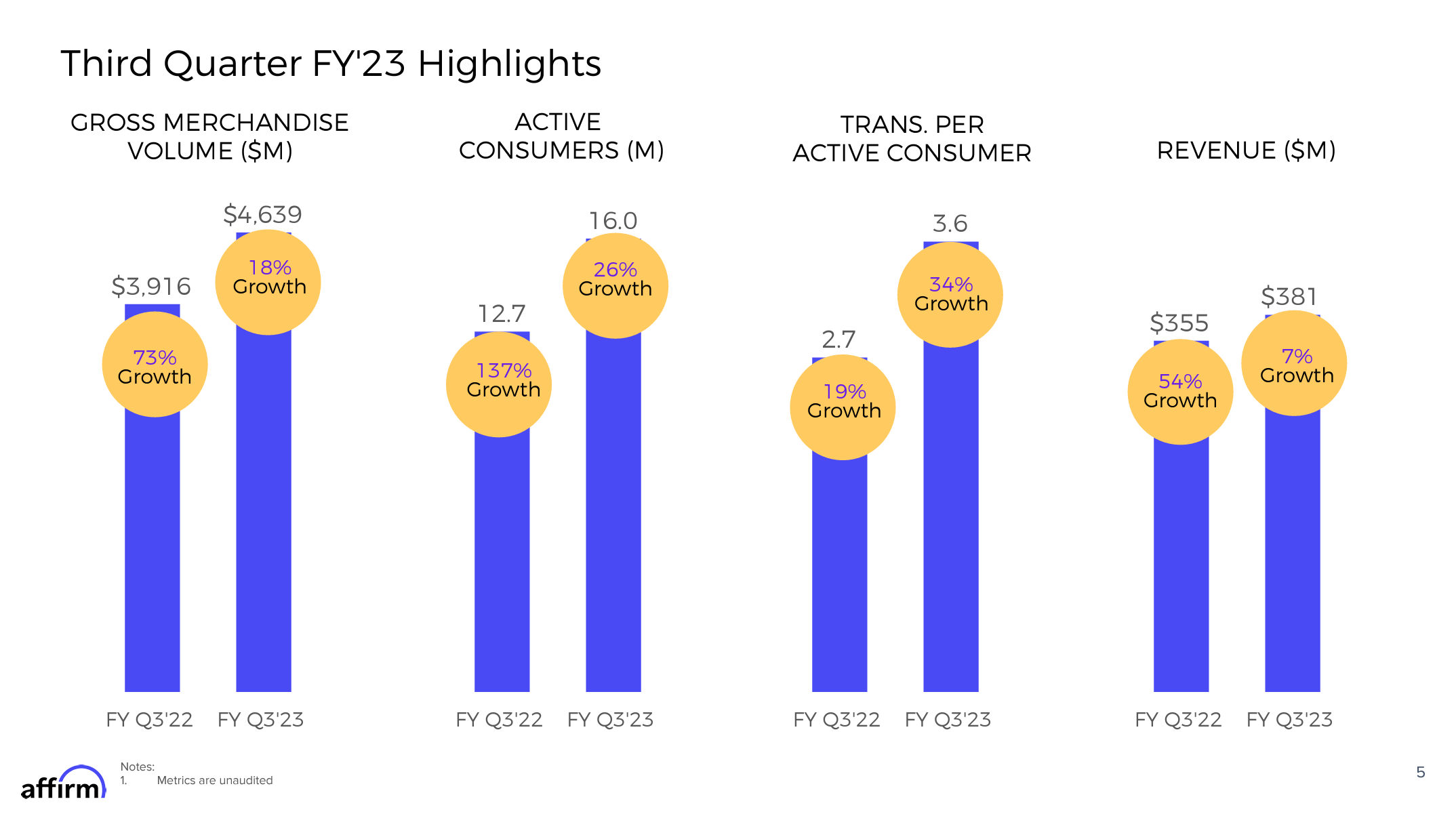

Buy now, pay later lender Affirm recently reported its earnings for the first three months of the year (Affirm’s FY Q3’23).

While the company posted a slight increase in top line revenue year over year, expenses grew more quickly, driven by rising cost of funds and spend on technology and data analytics.

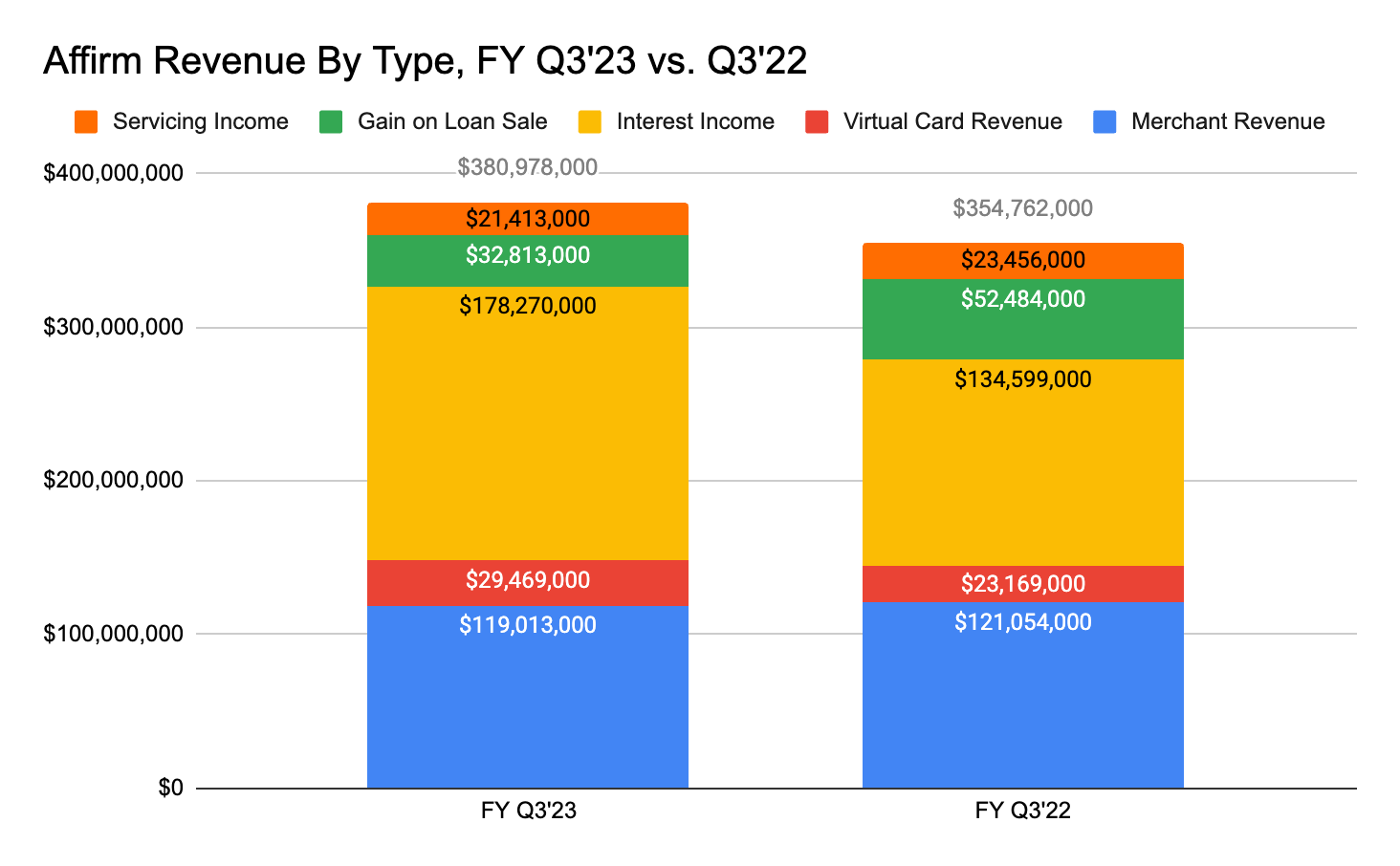

Merchant Revenue Declined, But Virtual Card And Interest Income More Than Made Up For It

On the top line, overall revenue increased by a modest 7.39%.

There were some notable changes to the composition of Affirm’s revenue, with revenue from Affirm’s merchant network dipping by 1.69% vs. FY Q3’22. Revenue from gains on the sales of loans declined about 37.5% year over year.

Those declines were more than offset by increases in interest income (+32.45%) and virtual card revenue (+27.19%) year over year. Rising rates are a tailwind for interest income, while Affirm’s strategy to diversify distribution away from dependence on merchants is showing up in the growing virtual card revenue.

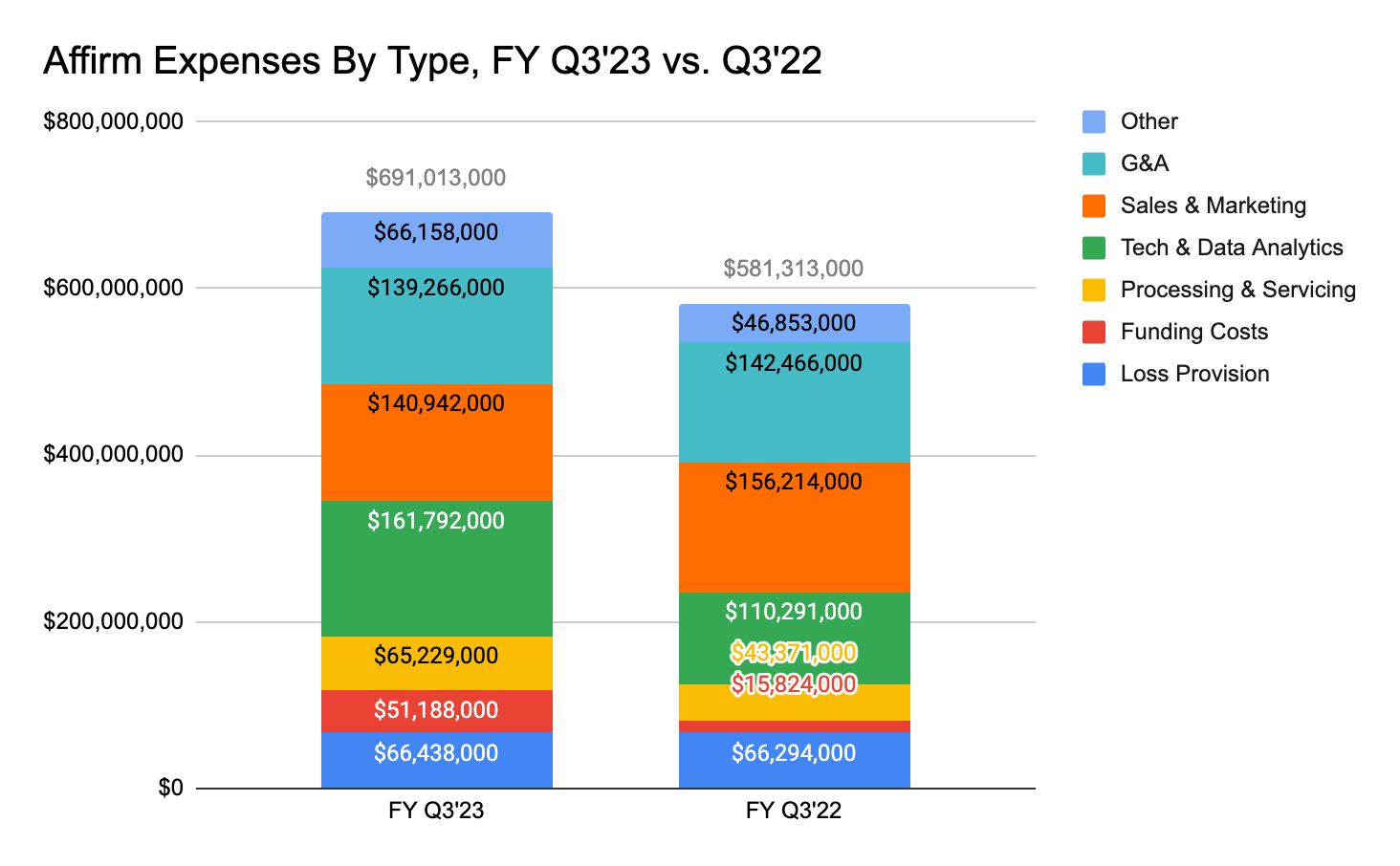

Funding Costs Jump 223% Year Over Year

On the expense side of the P&L, provisions for loan losses were essentially flat year over year.

Funding costs, however, saw a huge jump: 223.48% year over year, owing both to a larger loan book but, more importantly, a rising rate environment. This compares to an increase in interest income of 32.45% year over year. Per Affirm’s 10-Q:

The increase was primarily due to higher benchmark interest rates, increased utilization fees and an increase of funding debt during the current fiscal year. Additionally, the increase is attributable to a larger volume of on-balance sheet loans being retained during the period.

Processing and servicing costs rose about 50%, while spending on technology and data analytics jumped 46.7%.

Affirm trimmed sales and marketing expenses by about 10%, though it hasn’t pulled back as significantly as many other consumer fintechs.

Affirm also recorded a one-time restructuring charge of just shy of $35 million related to layoffs it conducted during the quarter. The company cut 19% of its workforce this February.

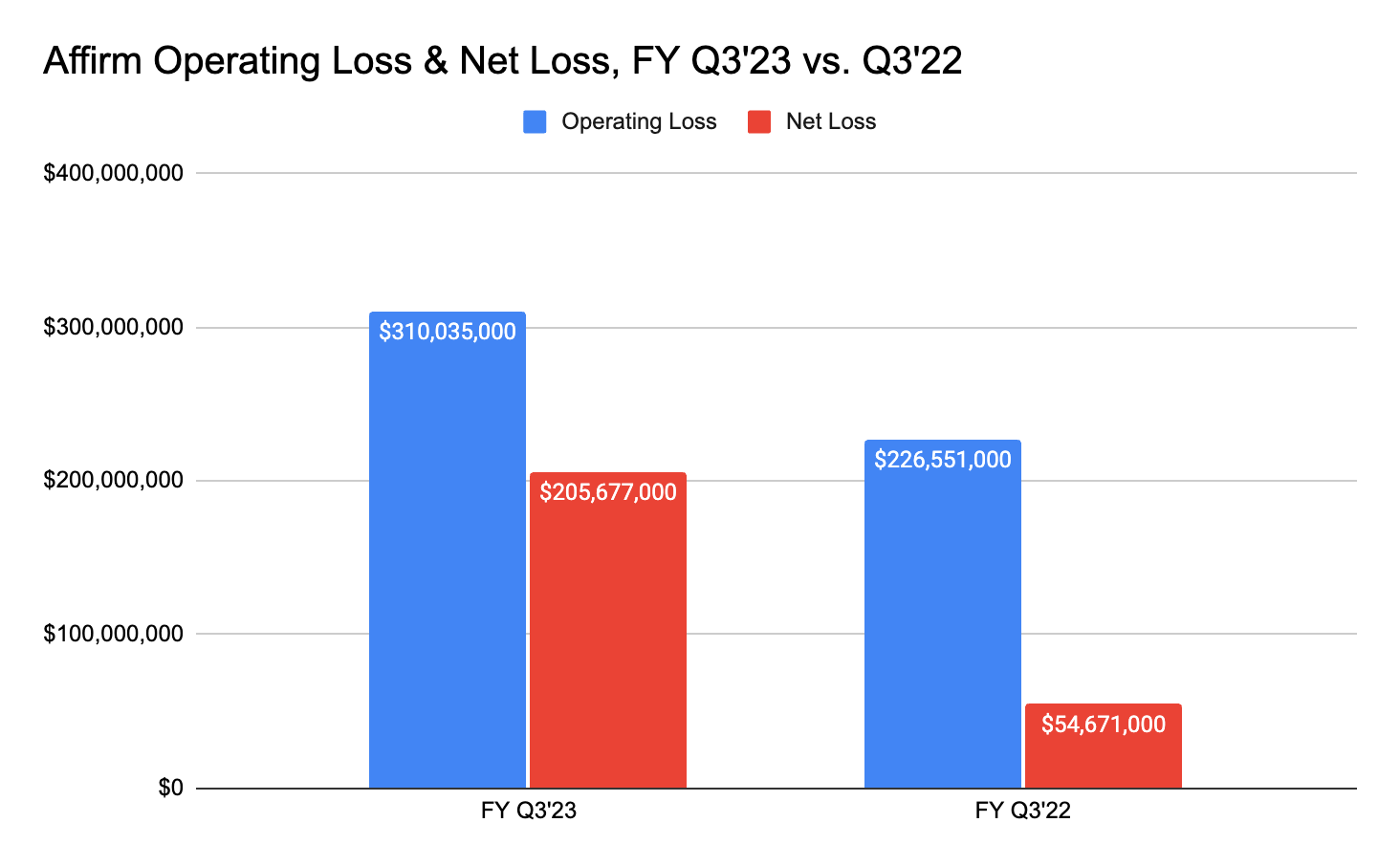

Net Loss Widens To $205 Million

The upshot is widening operating and net losses for the company. Affirm’s operating loss jumped about 37% year over year, while its net loss grew by 276%.

The “other income” component is the major driver of the difference between operating losses and net loss.

This item includes interest earned on Affirm’s cash and cash equivalents, recognition of gains on the early extinguishment of debt the company had issued, any changes in the fair value of interest rate derivatives, changes in the fair value of performance fee liabilities, changes in the fair value of residual trust certificates, changes in the fair value of the portion of securitized loan portfolios that Affirm retains, changes in the fair value of contingent consideration tied to its acquisition of PayBright, and other items.

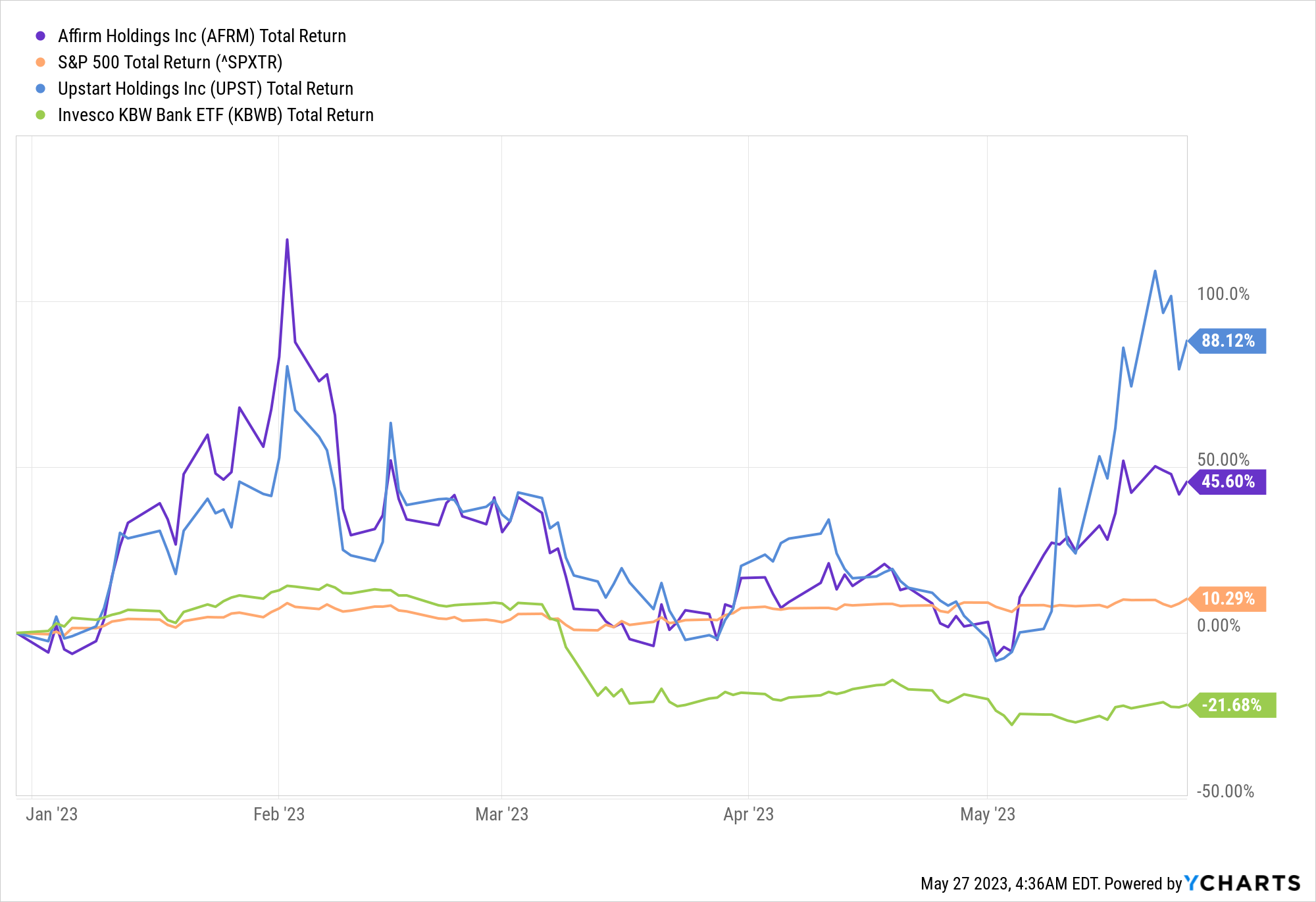

Affirm Outperforming Banks, But Underperforming Upstart

Despite the turmoil in the wider financial sector, Affirm has actually seen its market cap rebound nearly 50% since the beginning of the year, from $2.8 billion in January to $4.163 billion as of Friday.

That’s significantly better performance than the KBW Bank Index, which is down 21.68% year to date, and the S&P 500, up 10.29% year to date — though it trails Upstart, a largely similar non-bank fintech lender, which is up almost 90% year to date.

Five Key Takes Aways From Fed’s Household Economic Well Being Report

The Fed recently released its Economic Well-Being of US Households report, and the picture it paints is stark.

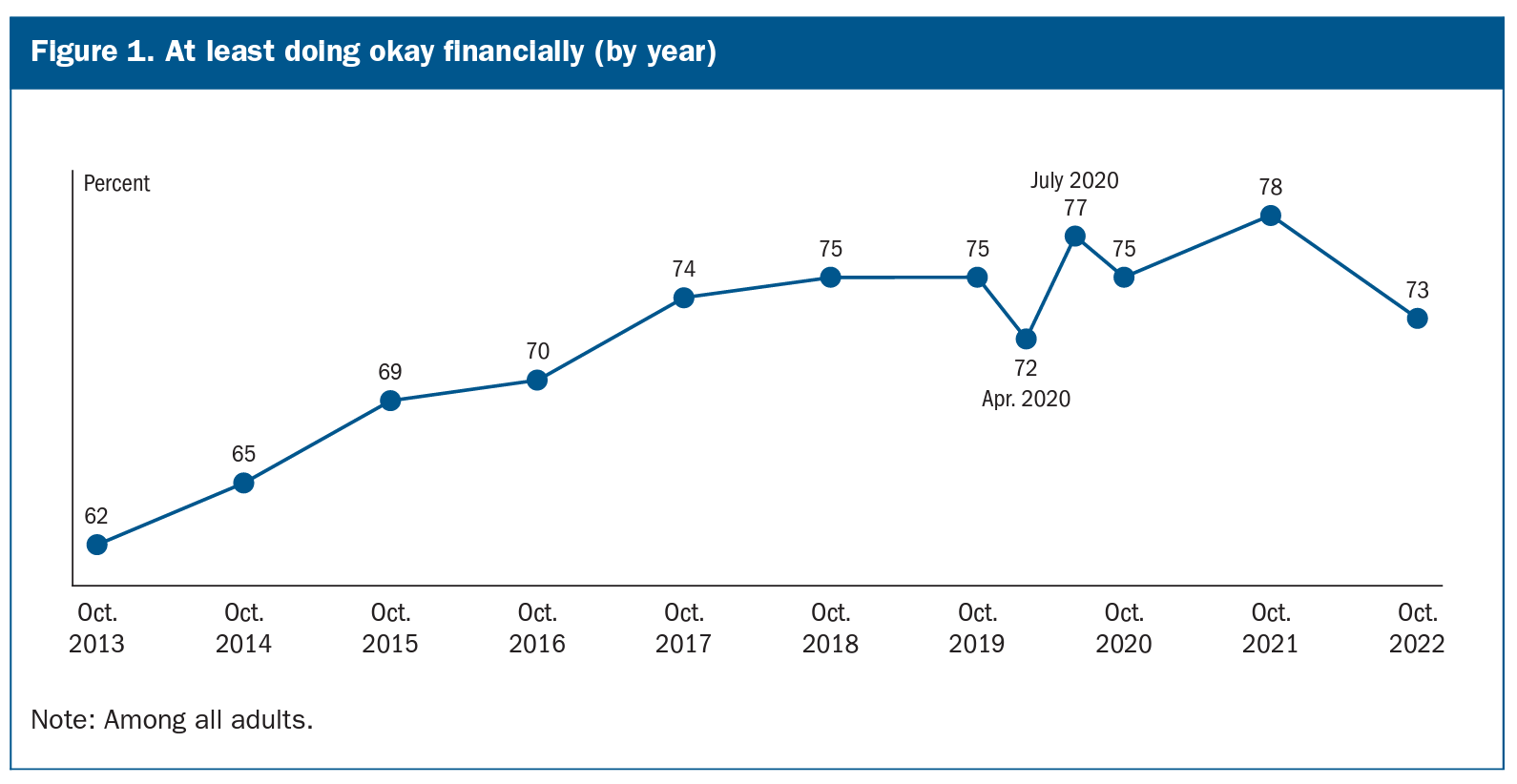

1. Households Overall Report Declining Financial Well Being

Overall, 73% of households reported they were “at least doing okay financially” — a 5 point drop from the year prior, and the lowest since 2016, apart from the early days of the COVID-19 pandemic:

Unsurprisingly, households with higher educational attainment reported higher rates of well being, with 88% of households holding a bachelor’s degree or higher reporting they were “doing okay” vs. just 49% of those with less than a high school degree.

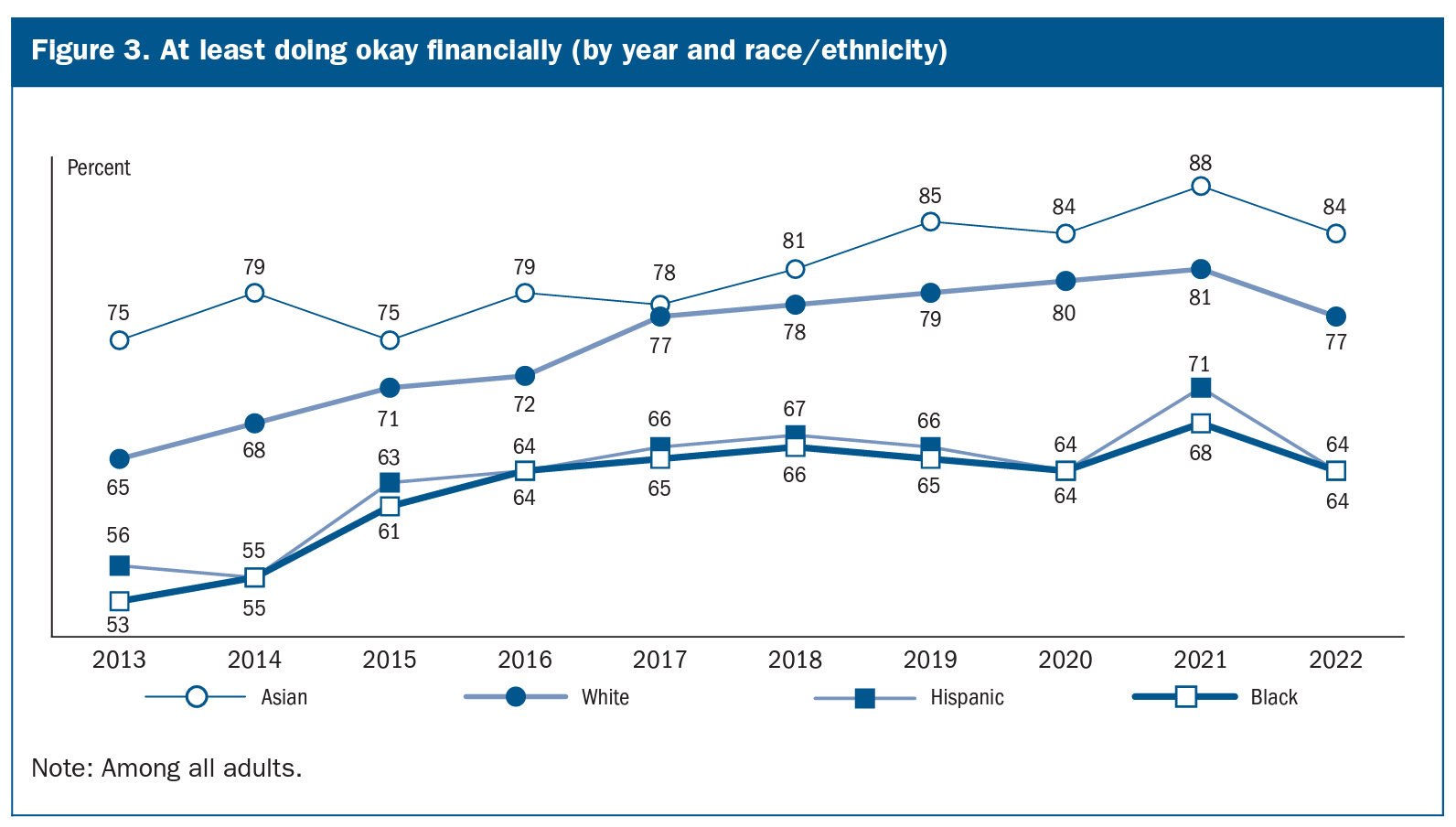

2. Black, Hispanic Households Report Lower Levels of Financial Well Being

Segmented by race/ethnicity, Black and Hispanic households reported significantly lower rates of well being, with 64% of both groups reporting they are “doing okay” vs. 77% of white households and 84% of Asian households.

All groups saw a decline from 2021’s peaks:

Beyond the headline numbers, the report contains a wealth of data across income, expenses, banking and credit, employment, housing, and education.

3. Expenses Outpace Income

Unsurprisingly, given the inflationary climate, increases in expenses outpaced income. Forty percent of respondents said their family’s monthly spending had increased, while just 33% said their income had increased.

The strong employment climate remains a bright spot. One-third of adults indicated they had received a raise or promotion in the year prior.

4. Declining Savings

With pandemic stimulus in the rearview mirror, households’ savings are dwindling. While in 2021 68% of households said they could meet a hypothetical $400 expense without borrowing, that proportion has declined to 63%.

5. High Banking Penetration, Low Crypto & BNPL Usage

Bank account adoption has been buoyed by a strong economy and pandemic-era stimulus measures, which encouraged those without accounts to get one.

The growth of no-fee fintech options, like Chime, Varo, and Cash App has likely helped foster adoption as well. In 2022, 94% of households reported having a bank account, though gaps remain by income, age, and race/ethnicity.

Crypto and BNPL, despite their high profiles, remain niche products. Just 3% reported using crypto, and 12% reported using BNPL in the year prior. Black and Hispanic adults were more likely than other groups to report using BNPL.

Colorado Bill Could Block High APR Fintech Lenders

The Colorado General Assembly has passed a bill that makes several changes to the state’s Uniform Consumer Credit Code, including opting the state out of certain amendments to the Federal Deposit Insurance Act. Jared Polis, the governor of Colorado, is expected to sign the measure.

Opting out of Sections 521-523 of the Depository Institutions Deregulation and Monetary Control Act (“DIDMCA”) is likely to lead to questions about the legality of loans above Colorado’s usury limit originated by out-of-state state-chartered banks to Colorado borrowers.

DIDMCA sought to normalize home-state interest exportation privileges between national banks and state-chartered banks. However, the act permits states to opt out of this provision.

And, while initially a handful of jurisdictions chose to do so, all but Iowa and Puerto Rico eventually allowed these opt-outs to expire. Iowa’s attorney general recently pursued a case against EasyPay, a BNPL provider, and its Utah-chartered partner bank, TAB, for violating the state’s 21% usury cap.

EasyPay and TAB ceased making loans in the state, and TAB subsequently saw its Community Reinvestment Act rating downgraded to “needs to improve” because of discriminatory or other illegal credit practices.

Now, it seems possible we’ll see similar cases in Colorado.

Legal analysts note that litigation on the topic is likely to hinge on whether or not loans are considered to be made “in” Colorado.

While much of the relevant legislation was written pre-internet, when it was substantially easier to determine where a loan was made, the question becomes somewhat murkier in the age of online lending.

Per a 1998 FDIC opinion, where a loan is made depends on the choice of law stated in the loan agreement and where the credit application approval, the extension of credit, and the disbursal of funds occurs.

While this certainly gives out-of-state lenders a robust argument that their loans aren’t made “in” Colorado, the state’s decision to opt out significantly increases uncertainty for fintech/bank partnerships offering loans above Colorado’s usury limit.

Daylight Shuts Down: Did We Really Need A LGBTQ+ Neobank?

Daylight is that latest neobank to call it quits. The startup had raised $20 million in equity from VCs that included Kapor Capital and Anthemis Group.

And while a recent exposé, revealing alleged questionable business ethics and problematic personal behavior by CEO Rob Curtis, surely didn’t help, the real problem seems to have been a lack of product/market fit: Daylight just didn’t solve (enough) problems for (enough) people.

While I was always skeptical of the likelihood of success of this niche neobank, its failure is unfortunate. At a time of escalating “culture wars,” typified by angry Bud Light drinkers shooting the beverage and shoppers threatening Target employees over Pride merch, representation still matters.

But, at least in this instance, representation wasn’t enough to build a viable business.

Some look at the size of the US LGBTQ+ community and their $1.4 trillion in purchasing power and see a huge TAM, but such analysis is reductive, boiling tens of millions of Americans down to a single characteristic — collapsing other attributes that may be more indicative of users’ financial needs and wants.

As a member of the LGBTQ+ community myself, I never understood why I would want to use Daylight vs. any other neobank or established financial institution.

Affinity plays like Daylight have ideally two key benefits vs. general market offerings: products and features tailored to their specific audience and more targeted, effective marketing, resulting in lower cost of customer acquisition. Daylight doesn’t seem to have achieved either of these.

While Daylight did offer some important, meaningful features, like enabling trans customers to use their chosen name, and attempted a late pivot toward focusing on family planning features, ultimately the company failed to gain meaningful traction before running out of runway.

Other Good Reads

Crypto Giant Binance Comingled Customer Funds and Company Revenue (Reuters)

JPMorgan’s US Debt Default Q&A (FT)

Daffy Launches Embedded Fintech Offering for Charitable Giving (Ron Shevlin/Forbes)

Seven Questions About the Future of Niche Neobanks (Fintech Takes)

About Fintech Business Weekly

🚨Act now to get 20% off my Banking-as-a-Service 2023 Market Analysis — offer expires Wednesday, May 31st🚨

Looking to work with me in any of the following areas? Email me.

Fintech advising & consulting

Sponsoring this newsletter

News tip or story suggestion — reach me on Signal at +1-316-512-1571

Early stage startup looking to raise equity or debt capital

Loved the write-up on the Colorado law change. Fintech leaders would be wise to monitor the state versus federal jurisdiction that is underway in many verticals in the industry.