a16z-Backed Crypto Startup: No Deposit Insurance is Feature, Not Bug; Experian's BNPL Bureau

Chime's Lending (& IPO) Plans, Acorns' Rotten SPAC, BaaS Primer, Crypto.com's $34m Hack

Hey all, Jason here.

There’s never a dull moment in fintech/banking/crypto. Even with some turmoil in the public markets, private fintechs continue to announce blockbuster funding rounds (though these were likely negotiated months ago). Still, as the Nasdaq slides into correction territory (and bitcoin along with it), it looks like 2022 may be a bumpier ride for the industry than years past.

Existing subscriber? Please consider supporting this newsletter by upgrading to a paid subscription. New here? Subscribe to get Fintech Business Weekly each Sunday:

a16z-Backed Eco Pushes ‘Benefits’ of Uninsured Deposits

A physical bank note is not the same kind of “money” as the balance in your checking or savings account.

The physical bank note is a direct claim on the central bank, whereas the balance in your checking account is a claim on the commercial bank holding that deposit.

I’d venture to guess that 99% of Americans don’t understand the distinction because, historically, they haven’t needed to. Even in times of significant economic turmoil, bank failures in the US are quite uncommon. And, when depository institutions do fail, depositors are protected.

They’re not just an unsecured creditor of a commercial bank, but protected by deposit insurance that ensures they will be made whole (up to a clearly stated cap of $250,000).

The deposit insurance and, perhaps more importantly, the prudential regulation of institutions that receive it, enable Americans to think of money in their checking account as “safe,” regardless of the specific bank holding it. As last week’s report on CBDCs from the Federal Reserve put it:

“Commercial bank money has very little credit or liquidity risk due to federal deposit insurance, the supervision and regulation of commercial banks, and commercial banks' access to central bank liquidity.”

Today, a user can be equally confident that their money is secure, whether held at Varo (a very small, unprofitable bank), Chime (not a bank at all, but with consumer deposits held at FDIC-insured partner banks), or JPMorgan Chase, the largest bank in the country.

Can you imagine if, when selecting a bank, consumers had to analyze the institution’s balance sheet and gauge the relative strength or riskiness of the bank’s assets vs. liabilities?

In practice, when storing funds in stablecoins, consumers are making a (probably ill-informed) bet on the stablecoin issuer to manage the safety and soundness of the currency by responsibly managing the assets backing it. But different stablecoins have different risk profiles — Tether (USDT) and Pax (USDP) stablecoins, both of which purport to be pegged in value to the US dollar, in fact have very different risk profiles.

Eco is not… FDIC Insured

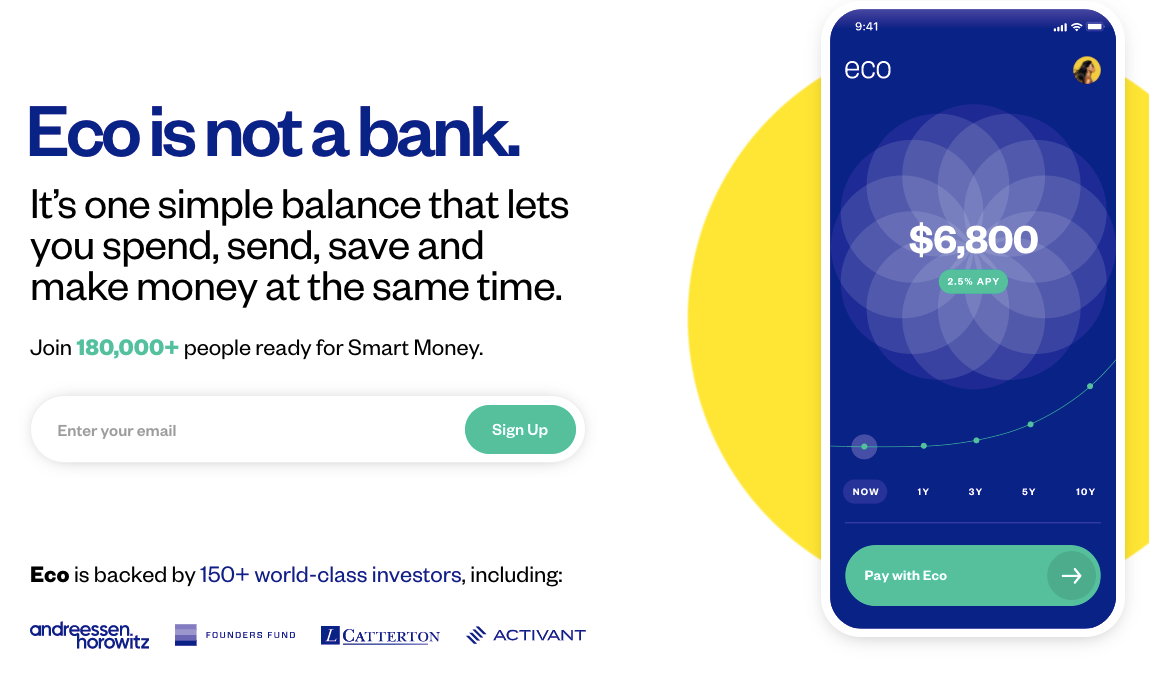

Enter Eco, a crypto spending account backed by some of the biggest names in venture capital, including Andreessen Horowitz (a16z), Founders Fund, Lightspeed Venture Partners, and Coinbase Ventures.

Eco cleverly positions itself as not a bank:

At the same time that it declares it is “not a checking account” and “not a credit card,” it directly compares itself to… checking and savings accounts and credit cards from companies like Goldman Sachs, SoFI, Bank of America, Chase, and Wells Fargo:

While one could argue that Eco has made clear that it isn’t these things — eg, it is not a bank, its product is not a checking account — by drawing direct comparisons to institutions that do offer those products, such positioning has the potential to confuse or mislead users about what the product actually is.

Beyond the statement that Eco is “one simple balance,” no where on its homepage does Eco affirmatively describe what its product is.

Who Really Needs Deposit Insurance Anyway?

To its credit, Eco’s homepage calls out key concerns potential users may have, though these clarifications are at the bottom of the page, rather than proximate to or referenced in relevant claims.

Concerns Eco identifies and aims to rebut include:

How does the 5% APY work?

What about the 5% cash back?

How does Eco make money, and is it sustainable?

How do people get comfortable without FDIC insurance?

Numerous DeFI-powered high-yield “savings” accounts have popped up that are less transparent about the nature of the product — that they’re not offering a “TradFi” product where deposits are insured; but rather that the USD a user sends to the platform is converted to a stablecoin, pooled with other users’ “deposits,” and lent out to third parties. The interest these borrowers pay is what generates the yield depositors receive (after the platforms take their cut.)

Eco argues that FDIC insurance doesn’t matter to most people, whether living paycheck-to-paycheck or highly affluent (emphasis added):

“As you might know, most Americans can’t come up with $400 in an emergency. As such, when deciding which financial service to use, they’re understandably much more concerned with the fees, how quickly they can get access to their money, and how the service can help them make every dollar they earn go as far as possible. Given the above, FDIC insurance almost never comes up, and if it does, it’s at the bottom of their list.”

The basic argument Eco is making here is that lower-income users are more worried about keeping the money they have (avoiding fees) than deposit insurance.

While it is certainly true that this customer segment is cost-sensitive, it is disingenuous to compare “fees” to “FDIC insurance” in a preference stack ranking.

New entrants to the financial system benefit from users’ assumption of safety and stability — an assumption built over decades from prudential regulation and, yes, deposit insurance.

Users are unlikely to rank FDIC insurance highly as a feature, because they may take for granted the safety and soundness of the traditional banking system that flows from it — and incorrectly assume that the same types of regulations apply to novel crypto-powered platforms.

Eco also potentially misleads by comparing itself to Cash App, pointing out that funds in the popular peer-to-peer payment app are uninsured.

The risk of storing funds in Cash App and the risk of storing funds via Eco are not the same. Were Cash App parent company Block to fail, users would become unsecured creditors, and, indeed, might not get all of their money back. That would be bad.

Users of Eco are similarly positioned. Were it (or its third-party custodians) to fail, Eco users may not get all their funds back.

But there is another risk; Eco converts users’ USD deposits into a USDC stablecoin. Users also take the risk, knowingly or not, that USDC could deviate from its peg to the dollar, a fact buried in the terms and conditions (emphasis added):

“Account balances held on the Eco Platform through Eco or directly or Third Party Services are held in USDC. While USDC is a “stablecoin” designed to remain pegged in value to the U.S. Dollar, and backed by U.S. Dollar reserves, Eco does not control the issuance, redemption or backing of USDC and cannot guarantee that 1 USDC will always remain redeemable for 1 U.S. Dollar.”

Eco further argues that users with ‘only’ $5,000 - $40,000 in their bank account don’t need deposit insurance, because they still spend the vast majority of each paycheck (emphasis added):

“Most in this group still live closer to “paycheck-to-paycheck” than you might think. They spend the vast majority (usually at least 80%) of their paycheck every month towards rent, transportation, food, health insurance, and other essentials.

Their bank balance of $5k-40k sits in their account and doesn’t change much — since they aren’t materially saving or earning interest. We make a point not to push people on moving their whole bank balance to start earning at Eco right away.

They usually start by using Eco for their monthly “money-in, money-out,” like they would have used cash back in the day. And with that volume, FDIC insurance doesn’t matter for them because it’s a relatively low dollar figure.”

I guess the argument here is that, at any given time, there isn’t a large amount of money in the account, and thus it doesn’t matter if it’s insured or not?

But that is the wrong lens by which to consider the question. It isn’t about the absolute money held in the account, but rather the impact on a user if these funds were lost.

If an Eco user is “paycheck to paycheck” and lost all of the funds they held with Eco, that loss would be significant, even if it’s a low absolute number.

If you only have $100 bucks that you need to pay rent, transport, food, or health insurance, and you lose it, it’s going to hurt, whether or not it’s a “relatively low dollar figure.”

The third category Eco argues doesn’t need to worry about deposit insurance are those ‘aggressively invested’ in the market (emphasis added):

“These people are already choosing to skip out on FDIC insurance in favor of trying to have their money work for them. They usually have as little in their checking accounts as possible. So the question never even comes up!”

This could be a misleading comparison. Users who deploy capital by buying stocks, bonds, or crypto aren’t “skipping out” on FDIC insurance. They’re making an investment, with hopes of earning a return in exchange for the risk they’re taking on.

In investing parlance, cash (or cash equivalents) is referred to as a “risk free” asset. The yield of US 10 year Treasuries is typically referred to as the risk free rate of return, because the likelihood of losing principal is essentially zero.

Conflating making a risk-bearing investment in search of earning a return with “choosing to skip out” on deposit insurance is a misleading comparison at best.

Finally, Eco rebuts the usefulness of deposit insurance for affluent users, who may hold in cash in excess of the $250,000 eligible for deposit insurance. Eco’s case to this audience is (emphasis added):

“When we ask them ‘why are you comfortable keeping so much money in your brokerage and in bank accounts where the majority of the balance isn’t insured,’ their response more often than not is simple: ‘if my banks go down, we have bigger problems.’”

This line of reasoning ignores the role deposit insurance plays in protecting the system in aggregate.

While a user holding $1,000,000 at Chase doesn’t directly benefit from deposit insurance coverage on $750,000 of that balance, the existence of deposit insurance (and the prudential regulation that goes along with it), regulates the amount of risk Chase can take on and, by fostering confidence in the banking system as a whole, protects it writ large.

The depositor with $1,000,000 balance is still benefiting indirectly from the systemic stability deposit insurance and regulation promote, even if a portion of their funds are uninsured.

No Mention of Security Risks

While Eco’s blog post goes to great lengths to convince users they don’t need deposit insurance, it’s silent on other risks that are fairly common in crypto (see Crypto.com story below) — including security breaches and hacks — though its terms and conditions spell out that such losses are ultimately borne by users (emphasis added):

“When you hold a balance in your Account, the applicable funds are held by a Third Party Provider. If such Third Party Provider suffers a security breach or other loss, you may suffer a loss of some or all of your Account balance.”

Products at the Intersection of Crypto and TradFi Will Benefit From the Clarity Well-Crafted Regulation Can Provide

It’s a cliche at this point to say that crypto is “the wild west.” And while it’s inaccurate to say companies like Eco are ‘unregulated’ — Eco holds MSB licenses and must adhere to KYC/AML regulations, for example — consumer-facing crypto lacks any crypto-specific regulatory framework.

Presumably, consumer protections, namely UDAAP, apply to companies offering products like Eco’s. But fundamental questions remain unanswered. Questions like:

What should these accounts be called? They’re not “bank” accounts. How should they be categorized, so as to avoid consumer confusion about what the underlying entity is and the protections it does (or doesn’t) offer?

This seems like something the team at Eco was cognizant of and struggled with; it defines the product in opposition to TradFi (“not a bank,” “not a checking account,”) but without ever saying what the product is!

To be fair, fintech suffers the same problem; Chime, which is not a bank, got in trouble with regulators for calling itself a bank. Now, it still calls itself a bank, but with a disclosure that says “Chime is a financial technology company, not a bank.” I’m guessing this isn’t doing much to clear up customer confusion. Not the best solution!

How can they be compared to TradFi products? Eco and similar products tend to explain the value propositions of their offerings by comparing them to established products a customer is likely to be familiar with.

As a marketing strategy, this totally makes sense!

But, it also seems likely to confuse users, if not done carefully, with clear and conspicuous disclosures. If you compare your “not credit card” to offerings from American Express, Chase, and Bank of America — without context on how the product is different from those offerings — it’s not unreasonable that a typical consumer could be confused:

How should users’ funds be described? Eco and other defi-powered yield products tend to use wording, imagery, and UX elements that make them look and feel like a user is holding “regular” US dollars (commercial bank deposits).

But they’re not; they’re typically holding a stablecoin — something that is not always clear to users.

While legislative and regulatory scrutiny is mounting on the sector, most the attention has been focused on potential systemic risks to the financial system — not on consumer protection.

At this point, it seems unlikely that we’ll see a serious effort at developing meaningful guidance on the rapidly growing intersection of crypto/defi and traditional finance until there’s a crisis or failure that results in every day consumers bearing significant losses.

Banking-as-a-Service Primer [Infographic]

The banking value chain and technology stack is being dis- and re-aggregated as technology rapidly evolves. This evolution is powering new models of creating and distributing products — impacting and enabling ecosystem stakeholders from established banks to fintech startups and even crypto to quickly launch new banking products and features.

While you’ll probably get five different answers if you ask five people, “What is banking-as-a-service,” it’s broadly understood to include making the building blocks of banking infrastructure available “as a service,” upon which others build product offerings.

Those building blocks range from narrow offerings, like an API-first card issuer-processor, to comprehensive ‘bank-in-an-API’ offerings, that offer nearly everything a company needs to launch a banking product, including an underlying bank license.

I’ve teamed up with my friends at Dutch fintech consultancy Fincog to put together an infographic overview of Banking-as-a-Service, including: what BaaS is, types of BaaS providers, the benefits of BaaS for fintech and incumbents, and how to go about selecting a BaaS provider.

Experian to Launch Specialty BNPL Bureau

Payments Dive is reporting that Experian, one of the “big three” credit bureaus in the US, is planning to launch a specialty bureau for buy now, pay later tradeline data.

According to Payments Dive:

“Experian said the specialty bureau, debuting in the first half of the year, will offer “a comprehensive view of consumer payments, including the number of outstanding BNPL loans, total BNPL loan amounts and BNPL payment status,” per the release.”

The specialty bureau approach differs from competitor Equifax, the first of the big three to announce its intention to enable BNPL providers to furnish data on pay-in-four products. Instead, Equifax has said it will use newly created classifications for the short-term financing products, but, by all indications, that data would reside in Equifax’s primary data stores.

Experian said it is choosing to create a distinct store for pay-in-four data to “protect consumer credit scores from negative impact.” Again from Payments Dive (emphasis added):

“Experian will store BNPL data separately, given that preliminary research shows that including all BNPL account information “can negatively impact consumer credit scores because of the way inquiries, new tradelines and utilization rates are reflected in credit score models,” Greg Wright, executive vice president and chief product officer for Experian, said in an email.”

This notably differs from Equifax’s analysis, which suggested some users could see a boost of up to 21 points to their FICO scores from inclusion of BNPL tradelines.

Secondary bureaus for specific types of products or credit data aren’t uncommon. Specialty bureaus for tracking data on payday loan usage have long existed — services like Clarity (acquired by Experian), DataX (acquired by Equifax), FactorTrust (acquired by TransUnion), MicroBilt, and TeleTrack.

How individual bureaus choose to incorporate data from BNPL providers may impact how a consumer’s score is calculated — a user’s score as derived from Equifax data, including BNPL products, is likely to be different (in either direction), than a score derived from Experian, that excludes BNPL tradeline data.

Consumers don’t have a choice of which bureau is checked when they apply for credit (and, in fact, many lenders pull data from more than one.) Such disparate treatment of how BNPL data is handled, and resulting discrepancies in credit reports and scores, is likely to drive consumer confusion and complaints.

$34 Million Vanishes, but Crypto.com CEO Says “No Loss of Customer Funds”

Cryptocurrency exchange Crypto.com suffered a hack last week that led to the unauthorized withdrawal of approximately $34 million worth of bitcoin, ethereum, and other currencies. A flaw in the company’s two-factor authentication (2FA) implementation seems to be to blame.

Upon detecting the unauthorized activity, the exchange froze all withdrawals for about 14 hours to prevent further theft of user funds.

What’s notable, beyond the theft and disruption themselves, is how the company and CEO Kris Marszalek responded — at first, describing the hack euphemistically as “an incident.”

Then, in an interview with Bloomberg TV, Marszalek stated (emphasis added):

“We very quickly stopped it, we paused withdrawals, we fixed it [and] we were back online about 13/14 hours and during the same day, all the accounts that were affected [were] fully reimbursed, so there was no loss of customer funds.”

The characterization that there was “no loss of customer funds” seems misleading at best. Customer funds were lost — thankfully, the amount was such that Crypto.com had adequate capital to reimburse them.

Other Good Reads

The End of Digital Transformation in Banking (Ron Shevlin/Forbes)

Money and Payments: The U.S. Dollar in the Age of Digital Transformation (Federal Reserve)

Why Facebook, Instagram and Twitter are embracing NFTs (Washington Post)

Crypto Giant Binance Kept Weak Money-Laundering Checks Even As It Promised Tougher Compliance, Documents Show (Reuters Special Report)

Contact Fintech Business Weekly

Looking to work with me in any of the following areas?

New: Product strategy or go-to-market consulting

Sponsoring this newsletter

Content collaboration or guest posting

News tip or story suggestion

Early stage startup looking to raise equity or debt capital

Feel free to reach out to me: jason@fintechbusinessweekly.com

Looking for the stories on Acorn’s SPAC and Chime’s Lending Plans?

There’s more Fintech Business Weekly below for paying subscribers👇 — if you already subscribe, thank you for helping make this newsletter possible