Hey all, Jason here.

This Sunday, I have a “hybrid” post for you — both regular newsletter content and a special podcast conversation about banking-as-a-service and regulation, with guests Sankaet Pathak, co-founder and CEO of Synapse, and Shaul David, Head of Banking at Railsr.

We had a wide-ranging conversation about the space, including:

How banking-as-a-service can help bank/fintech partnerships to scale

Why some banking-as-a-service platforms want to be regulated

How to ensure customers funds are protected when a fintech (or bank, or e-money institution) fails

Predictions for the future of banking-as-a-service

and more

Click “Listen Now” above or find the show on Apple Podcasts, Google Podcasts, Spotify, or anywhere else you listen to pods.

Existing subscriber? Please consider supporting this newsletter by upgrading to a paid subscription. New here? Subscribe to get Fintech Business Weekly each Sunday:

How Do Goldman Sachs’ CFPB Complaints Stack Up?

Last week, we learned that the CFPB is investigating Goldman Sachs, which issues co-branded cards with Apple and General Motors, over its “credit card account management practices, including with respect to the application of refunds, crediting of nonconforming payments, billing error resolution, advertisements, and reporting to credit bureaus.”

Now, CNBC is reporting one possible source of the scrutiny is how Goldman handles chargebacks on its cards. Per CNBC (emphasis added):

“When an Apple Card user disputes a transaction, Goldman has to seek a resolution within regulatory timelines, and it sometimes failed at that, said the people, who requested anonymity to speak candidly about the situation. Customers were sometimes given conflicting information or had long wait times, the people said.

Goldman got more disputes than it counted on, said one source. ‘You have these queues that you need to clear out within a certain amount of time. The business was getting so big, suddenly we had to create more automation to deal with it.’

…Regulators are focused on customer complaints from the past few years, and the biggest source of those came from attempted chargebacks…”

The Fair Credit Billing Act (FCBA) requires card issuers to acknowledge receipt of a dispute within 30 days and to investigate and resolve them within two billing cycles (not to exceed 90 days).

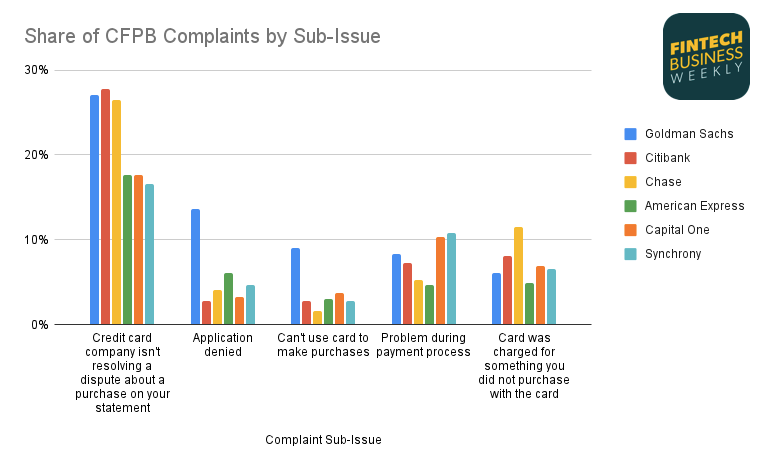

Goldman Sachs’ Most Common Complaints

Since launching its first credit card, the Apple Card, in August 2019, consumers have lodged just over 1,300 complaints related to Goldman’s credit cards with the CFPB.

While it is difficult to compare Goldman to other issuers on the absolute number of complaints, it’s possible to compare the relative frequency of types of complaints.

Since the launch of the Apple Card, the five most common categories of complaint about Goldman to the CFPB were:

Credit card company isn't resolving a dispute about a purchase on your statement

Application denied

Can't use card to make purchases

Problem during payment process

Card was charged for something you did not purchase with the card

So how does Goldman stack up to other major card issuers?

About 27% of all complaints to the CFPB about Goldman’s credit cards were related to transaction disputes. While this may sound high, it’s slightly below major card issuer Citibank, though above American Express, Capital One, and Synchrony.

A typical complaint to Goldman about a dispute sounded something like this one (emphasis added):

“I had made a purchase at a XXXX dealership for a service ( fixing my a/c ). I paid for the service up front, like the dealer requested. I had to leave town for work, when I came back the dealer sent back the parts for my car, so I spoke to the XXXX and he agreed to refund me for the services, given that I never received them. XXXX never refunded me, so I took it with XXXX XXXX Credit Card and dispute it.

They returned saying that the dealership had enough proof that I made the purchase. However they refused to see that through the whole time I talked to them about the dispute, I mentioned several times, I never received the service. I made the purchase and never got the services. When requested proof of the investigation. They had none, only that I made the purchase. No proof of the dealership saying I received the services, the only thing I got was we can do nothing.”

The two categories of complaint where Goldman really stands out from others are “Application denied” and “Can’t use card to make purchases.”

The high share of complaints about denied applications makes enough sense, given the high-profile launch of the Apple Card and unfounded complaints of gender discrimination.

The complaints about not being able to use the card to make purchases — which accounted for just over 9% of all complaints about Goldman-issued credit cards, are a bit more unusual. For other major issuers, these kinds of complaints represented just 2-4% of complaints to the CFPB.

Though the exact complaints vary, a common theme emerges, where a user’s card is restricted for unclear reasons, and, when they contact Goldman, they’re unable to get an answer as to why.

Many complaints also referenced calling repeatedly, long hold times, and unfulfilled promises that consumers would be called back.

For example, one customer wrote to the CFPB (emphasis added):

“For exactly a month now, Apple restricted my Apple credit card and I have not been able to make purchases using this card because they said my account is ‘under review’.

They said that someone would contact me to resolve the situation when the review is done, but they never did. When I tried calling back like every week (latest was on XX/XX/XXXX), Apple still told me the same thing ... to wait for a return call.”

…and another wrote (emphasis added):

“I used my credit card within my limit as I normally would. The account has been restricted and I wasnt told why other than something triggered a response in their department. Ive called numerous times and my account is still restricted over a week later. Im not given a time frame of when I can usee my account. After reading about this companys practices online in similar cases, it looks like many people are restricted from using their cards for over a month.”

CFPB Interpretative Rule Puts Google, Meta on Notice For UDAAP, Consumer Protection Violations Liability

The CFPB has put “Big Tech” on notice that they may be considered service providers to financial services companies that use their advertising platforms and thus “can be held liable by the CFPB or other law enforcers for committing unfair, deceptive, or abusive acts or practices as well as other consumer financial protection violations.”

The CFPB’s statement released in conjunction with the interpretative rule draws a distinction between “traditional advertising,” like a TV commercial or bill board, and “digital marketing.” According to the statement (emphasis added):

“Traditional advertising relies on getting a product or service out to as wide an audience as possible. A traditional marketer, for example, may try to purchase time and space for a TV commercial on the most watched station or show.

Digital marketers, on the other hand, seek to maximize individuals’ interactions with ads. They may harvest personal data to feed their behavioral analytics models that can target individuals or groups that they predict are more likely to interact with an ad or sign up for a product or service.”

Because digital marketing platforms “go beyond” traditional advertising, they do not qualify for the “time and space” exception that a TV station or newspaper would enjoy, the CFPB says.

The agency argues that targeting and optimization algorithms common in digital marketing constitute a material service to financial advertisers (emphasis added):

“Digital marketing providers are typically materially involved in the development of content strategy when they identify or select prospective customers or select or place content in order to encourage consumer engagement with advertising.

Digital marketers engaged in this type of ad targeting and delivery are not merely providing ad space and time, and they do not qualify under the ‘time or space’ exception.”

What does this mean in practice? While the CFPB doesn’t name specific ad platforms in the interpretative rule nor in its statement, it’s pretty clearly targeted at Google and Meta (Facebook).

While the statement about the interpretive rule is broad, referencing potential liability for unfair, deceptive, and abusive practices, the most obvious area that could receive scrutiny is how ad platforms ensure compliance with ECOA or other kinds of unfair discrimination.

The Equal Credit Opportunity Act prohibits discrimination in access to credit on the basis of race, color, religion, national origin, sex, marital status, age, public assistance, or the exercise of any rights under the Consumer Credit Protection Act.

This isn’t purely theoretical — the Department of Justice recently reached a settlement with Meta on similar allegations that when its targeting algorithms were used for housing advertisements, the result was illegal discrimination in violation of the Fair Housing Act.

In fact, CFPB Director Chopra referenced this case in remarks he gave last week coinciding with release of the rule. He closed those remarks by saying (emphasis added):

“Today, relationship banking is under threat. In part, this is because our sensitive data is viewed as more valuable to firms than our actual selves. Advances in technology should help our economy and society advance, rather than incentivizing a rush to seize our sensitive financial data and to allow tech giants to evade existing laws that other firms must comply with. It is critical that we all work together to address this.”

Digit to Pay $2.7 Million Penalty for Deceiving Users on Overdrafts

Savings app Digit, which was recently acquired by small-dollar lender Oportun, has reached a settlement with the CFPB over its marketing and business practices that resulted in consumers overdrafting their accounts.

The language in the press release announcing the order is notable for describing the company as “lying” to consumers:

The Digit app links to a customer’s existing checking account and then automatically determines an amount to transfer to a separate savings account.

Digit promised that such transfers would not cause a user to overdraft their account and that, if they did, Digit would reimburse them.

But, according to the consent order, that was not the case:

“Falsely guaranteed no overdrafts: Hello Digit represented that its tool “never transfers more than you can afford,” and it provided a “no overdraft guarantee.” But instead, Hello Digit routinely caused consumers’ checking accounts to incur overdraft fees charged by their banks. Hello Digit received complaints about overdrafts daily.

Broke promises to make whole on its mistakes: The company also represented that if there was an overdraft, it would reimburse consumers. But the company often denied customers who tried to recoup their money. The company has received nearly 70,000 overdraft-reimbursement requests since 2017.

Pocketed interest that should have gone to consumers: As of mid-2017, Hello Digit deceived consumers when it represented that it would not keep any interest earned on consumer funds that it was holding, when in fact the company kept a significant amount of the interest earned. Had Hello Digit kept its promise to not keep the interest on consumers’ funds, consumers could have pocketed the extra savings.”

For its part, Oportun, which acquired Digit, released the following statement (emphasis added):

“Digit received a CID from the CFPB in June 2020. The CID was discussed with Oportun during the acquisition process. The stated purpose of the CID was to determine whether Digit, in connection with offering its products or services, misrepresented the terms, conditions, or costs of the products or services in a manner that is unfair, deceptive, or abusive.

Through the investigation, it was found that with a success rate of better than 99.99%, Digit isn’t ‘perfect,’ meaning a Digit Save transaction caused an overdraft fee for one of our members less than 0.008% of the time.

As a result, Digit owes 1,947 members approximately $35 each, for a total of $68,145. In addition, Digit will pay a civil money penalty of $2.7 million. While we disagree with the CFPB on this matter, we are happy to have it settled.”

It’s unclear how Digit’s purported 99.99% success rate reconciles with the CFPB’s claim that the company has received nearly 70,000 overdraft-related complaints since 2017.

Other Good Reads

What’s Going Wrong at Goldman Sachs’ Marcus Consumer Bank (Business Insider)

A PFM App By Any Other Name (Fintech Takes)

Family Fortunes: The Origins and Growth of the Family Office (Net Interest)

Contact Fintech Business Weekly

Looking to work with me in any of the following areas? Email me.

Fintech advising & consulting

Sponsoring this newsletter

News tip or story suggestion

Early stage startup looking to raise equity or debt capital

Banking-as-a-Service & Regulation: A Conversation with Sankaet Pathak of Synapse & Shaul David of Railsr